News

News

FTFL - The Other 97%

This article appeared in our September 2025 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

We are big fans of the AI Daily Brief podcast. A recent episode discussed whether AI is a bubble or a boom, using this article by tech entrepreneur and author Azeem Azhar as a guide. We start this month’s FTFL by building off of Azeem’s analysis to share some bubble indicators we found interesting. Later on below we shift gears and discuss what all this AI craziness means for the forgotten companies that are NOT developing AI technology (there’s a whole lot of them).

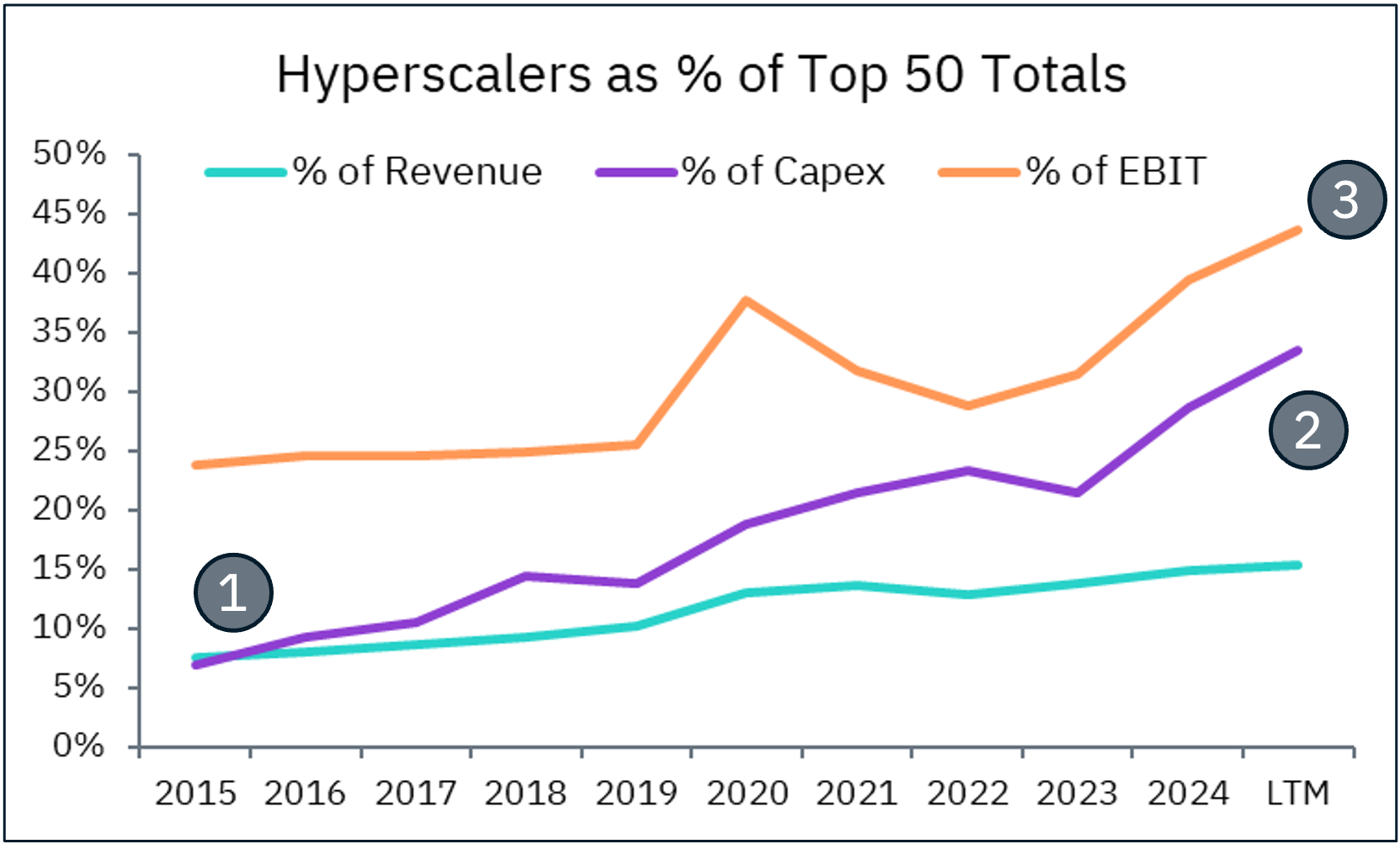

First, we focus on the top 5 hyperscalers feeding the AI bubble: Amazon, Apple, Google, Meta and Microsoft. It’s no secret they are spending massive amounts of capex on data center buildouts to keep up with AI computing demand. Is all that spend overtaking the economy at large? In the chart below, we took the top 50 global companies by revenue, and tracked hyperscaler financial metrics relative to the whole group over the last 10 years.

In 2015, both hyperscaler revenue and capex were about 7% of their respective totals from the top 50 (1). Since then hyperscaler capex has increased much faster, now representing 33% of the top 50 capex (2), vs. revenue at 15% of the total. We might think that feels very bubblish, as capex can’t outpace revenue forever. But then we look at the hyperscalers’ EBIT over the last 10 years. Already representing 24% of aggregate EBIT in 2015, hyperscaler EBIT share is now an astounding 44% of the total top 50 (3). Market power concentration concerns notwithstanding, that kind of return on investment indicates at least a strong foundation for otherwise staggering growth. And it’s worth noting that this AI investment is driven by companies principally reinvesting their own cash flow (not external investment) into buying Nvidia GPUs.

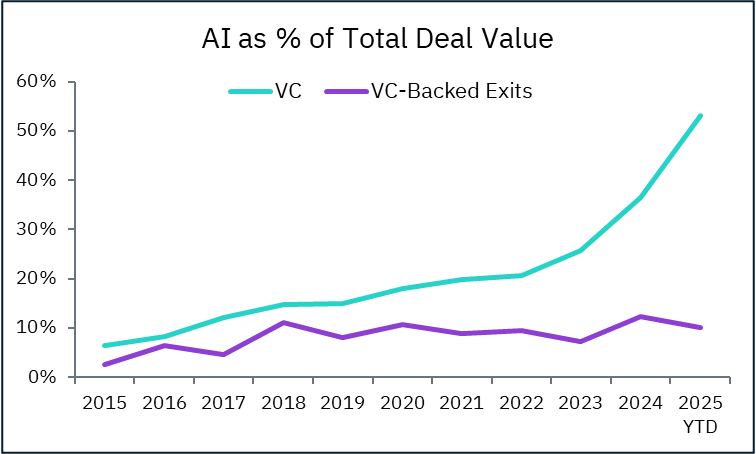

Switching to another aspect of the bubble/boom, let’s see how much AI has powered the global deal market, namely VC funding rounds and VC-backed exits.

As we’ve discussed before, AI is overtaking global venture funding rounds, now up to 53% of all VC dollars invested. But we’re not seeing it come out the other end just yet. AI is only 3% of VC-backed exits, creating a significant and fast-growing backlog (hello, 2028?).

That 3% means a whopping 97% of VC-backed exit value is coming from the others, the forgotten, the non-AI.

Since the public launch of ChatGPT in November 2022, there have been 130,000 companies worldwide that have received venture funding, of which 30,000 are AI companies, leaving 100,000 companies vying for attention. We can even add to that group the 18,000 AI companies that were founded before 2022, and are likely already viewed as “old” tech. Suffice it to say, the mass of AI investment has created an island of forgottens. But when it comes to exits, the inverse is true.

At Bowen we view ourselves as sellside sherpas, so to this large group of “others”, we’d like to offer some guidance as you navigate the trails ahead:

- Valuation rising tide – while Anthropic’s Series F at 34x revenue may not be directly applicable to you, we believe there are far-ranging downstream effects. We notice that the Nasdaq-100 is currently at a P/E ratio of 32x, pretty much the same level as the post-pandemic period that kicked off the 2021 exit frenzy.

- Prioritize profitability over growth – as a general rule, we advise executing towards maximizing YoY growth. As a non-AI company – with all of the current capital and presumably future capital flowing to AI – you must exhibit self awareness and extend your runway and that means reducing your burn. Simple math, if you have the option of spending heavily to grow 30%, or growing 15% and achieving a path to breakeven, choose the slower growth option.

- Look for silver linings in AI clouds – use those ever increasing AI investments to enhance your ability to cut costs. Agentic AI will soon be enterprise wide. Don’t be the last to adopt it. In fact, be the first.

- Reverse buyside – our friend Ronan Kennedy of B Capital coined this concept and it is an important one. Too many companies that are non-AI spend far too much time worried about oversharing with the market, the community, their competitors. This behavior pattern results in teams and technology which are undermarketed best case, or unknown worst case. If this is you, it will take 18-24 months to sell your company. Engage with your near peers, competitors and likely acquirers and you should be able to successfully sell in 6 months.

- Play it forward – taking private stock in a transaction is not the end of the world. From unicorns doing secondary buyouts to PE rollups reaching a tipping point, we are seeing a lot of near-term liquidity opportunities in rollovers and private mergers. Be judicious about cash versus stock and conduct reverse due diligence, but don’t say you will not consider an overvalued unicorn as your exit partner. It might be the worst – and prevent you from the best – decision you ever made!

If all of this – or any of this – makes you uncomfortable, news flash: you are living in the era of AI. Get comfortable being uncomfortable is our best advice.