News

News

FTFL - All-in on AI

This article appeared in our September 2024 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

Not a day goes by that we don’t hear about how VCs are spending all their time and money on AI (as in, just yesterday). So here is our take, curated for our growth tech audience.

To better visualize the massive impact that AI is having upon the entire venture landscape, consider that venture investments were down from a high of $877 billion in 2021 to $370 billion in 2023, a decline of 58%. With AI investments now making up 32% of all venture investing (1) – up an astounding 2x from just 2 years ago – venture investments in 2024 miraculously appear to be on track to reverse the declines.

Underneath this data lies something far more interesting and potentially sinister – Megadeals, or $100M+ VC rounds. AI Megadeals have accounted for 21% of all VC activity (2) in 2024 YTD, headlined by Anthropic’s $1.2B Series D, Scale AI’s $1B Series F, and Mistral AI’s $651 Series B. Why do we consider megadeals to be sinister? Because less than 4% of all funds classified as “venture” can write checks large enough to participate. This means that the vast majority of funds must find another way to create traditional LP returns – keep reading!

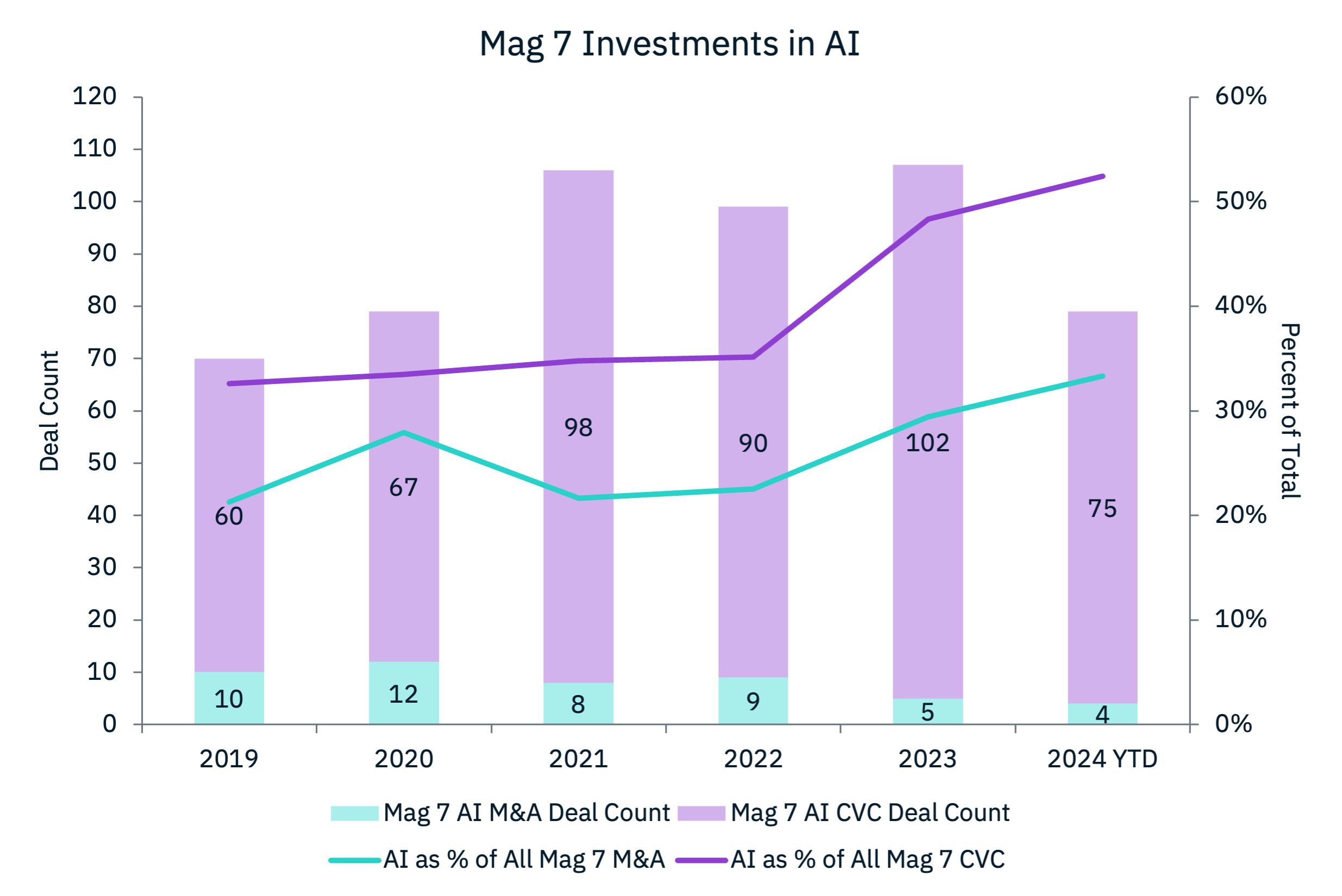

It’s not just VCs fawning over AI. We’ve seen another group significantly open their wallets to AI – the Magnificent 7.

Mag 7 AI investments are on the rise, and currently represent 52% of all Mag 7 investing. Looking at dollar amounts, funding rounds in which the Mag 7 have participated are now overwhelmingly focused on AI, representing 75% of all investment dollars with Mag 7 participation.

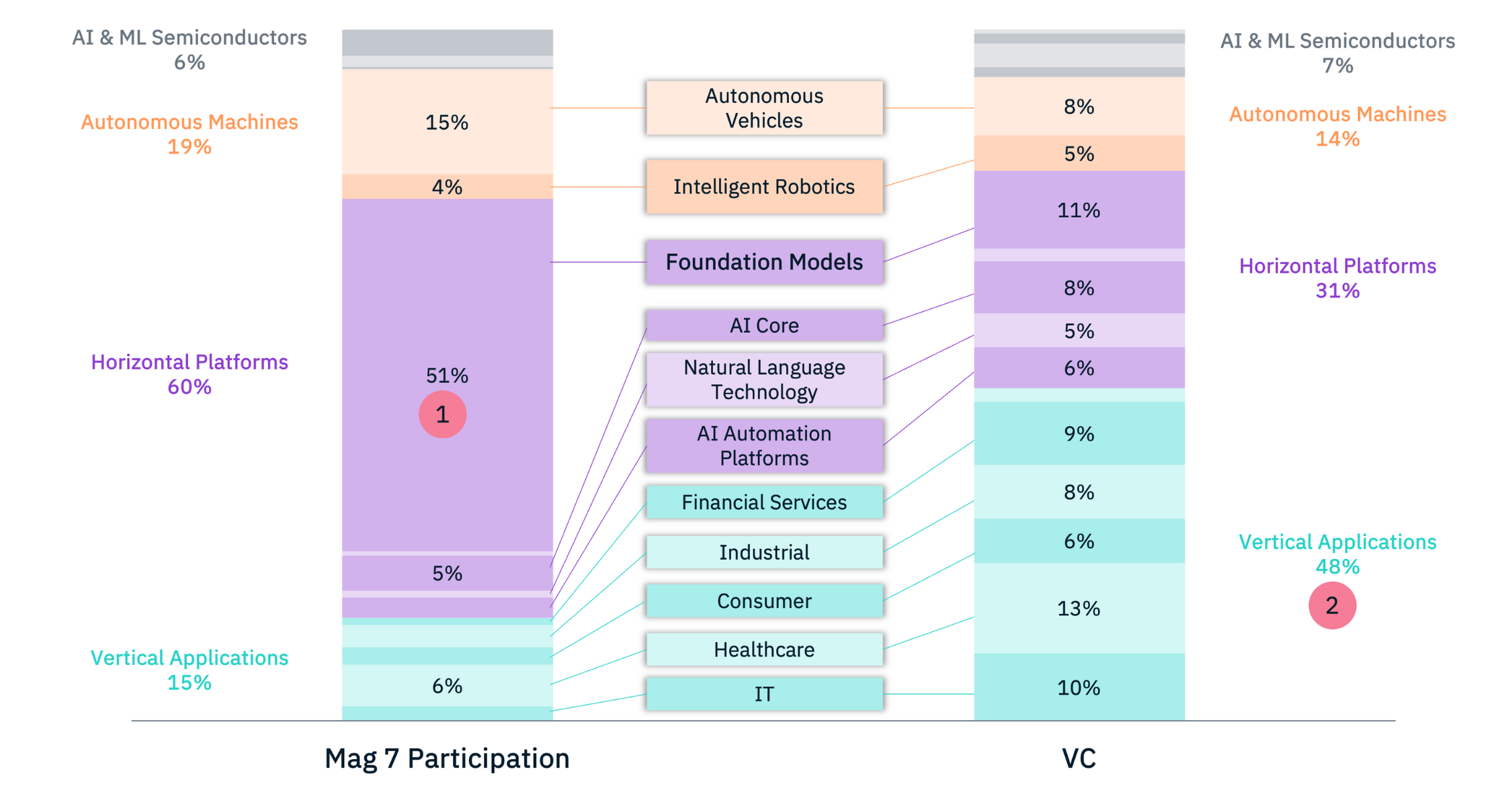

Next, we looked at Mag 7 and VC capital invested across AI subsectors since 1/1/22. It would seem that an industry famous for encouraging its participants to “pivot” has, in fact, pivoted itself.

Clearly what stands out is the discrepancy with Foundation Models (1). The Mag 7 are disproportionately making big bets on companies like OpenAI, Anthropic and Databricks, fueling the war for AI building block supremacy. In fact, many of the AI Megarounds we mentioned earlier were led by the Mag 7 (hat tip to CNBC for scooping us by a few days).

Meanwhile, VCs, unable to compete with the Mag 7’s check sizes but still aggressively funding AI companies, have moved up the stack (2), with nearly half of AI funding going to Vertical Applications ($124B since 1/1/22). VCs are betting on companies that will leverage Mag 7-funded infrastructure to solve specific business problems – without having to buy their own Nvidia GPUs. Example recent investments in Vertical Applications include $62M for Bright Money (Financial Services), $50M for Cohere Health (Healthcare), $40M for Torq (IT), and $68M for SafeAI (Industrial).

Just like the dotcom and cloud booms before it, AI has created a tectonic shift in the venture investing landscape. To wit:

- The Mag 7 are the new SoftBank (and have been forced to do some wacky transactions as a result)

- Oracle is now relevant again – Larry Ellison hasn’t lost a step at 80

- The 96% of funds sidelined by Megadeals appear to have pivoted and may well be in the early stages of charting their own path to AI riches

- …As long as we don’t run out of energy first

But wait, we haven’t mentioned M&A yet – odd for an M&A specialist. You may have noticed in the second graph that the Mag 7’s AI acquisition deal count is down ~50% from a few years ago. It makes us wonder, if Megadeals are increasing, and our biggest buyers are buying less, who will actually acquire these AI companies?