News

News

FTFL - The 7-Year Itch

This article appeared in our January 2024 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

At this stage of 2024, we are confident you have read, re-read, and been thoroughly depressed by the dozens of articles on how difficult the venture-backed liquidity environment was in 2023.

As we dive into January’s FTFL, we asked ourselves: By historical standards, was it really that dire? And when, oh when, will it get better?

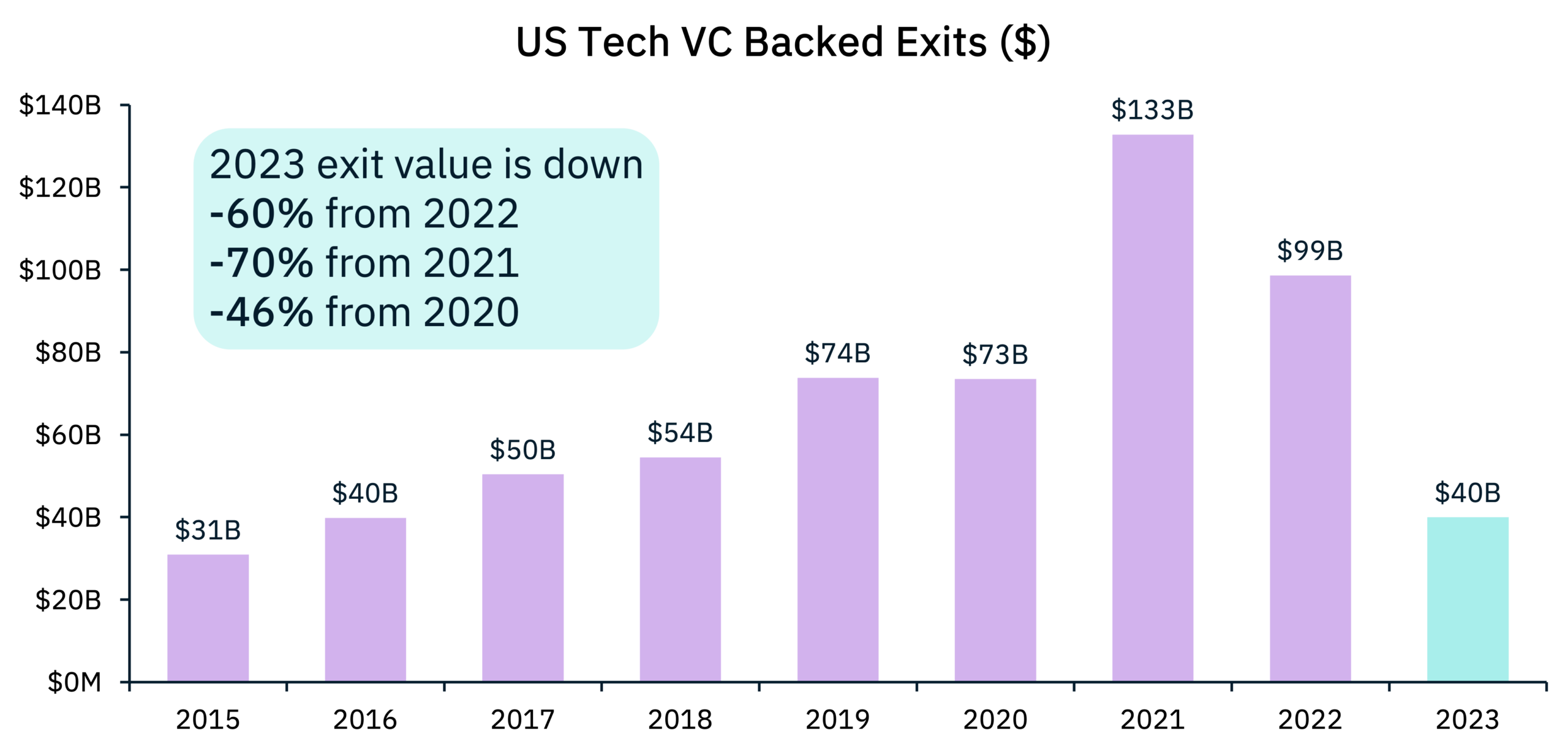

Not only were M&A and IPO proceeds down 70% from the 2021 high, they were down 46% from the baseline levels of 2019-2020. The last time exit values were this low was in 2016. Compare this to historical CAGRs of 10-15%. There’s no sugarcoating it – in the immortal words of Queen Elizabeth II, 2023 was an annus horribilis for venture-backed companies.

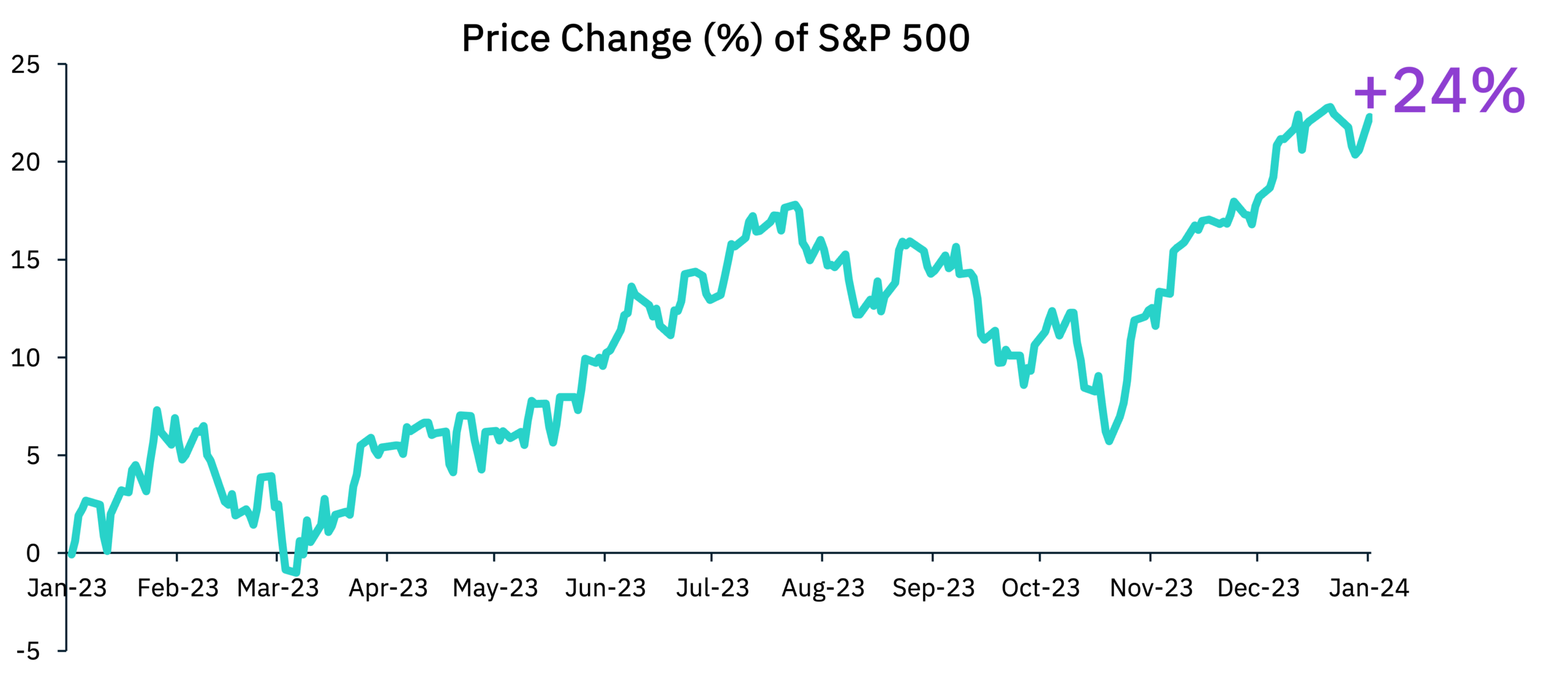

But how do we square these lowly stats with what appears to have been a red-hot stock market?

One part of the answer is that private markets always lag the public markets. Whenever public market valuations change, it takes private markets 2 to 6 quarters to align with the updated valuation environment.

But that doesn’t necessarily mean the exit environment will start coming back in 2H24… the other part of the answer is the hidden dynamic in the S&P 500’s gaudy performance:

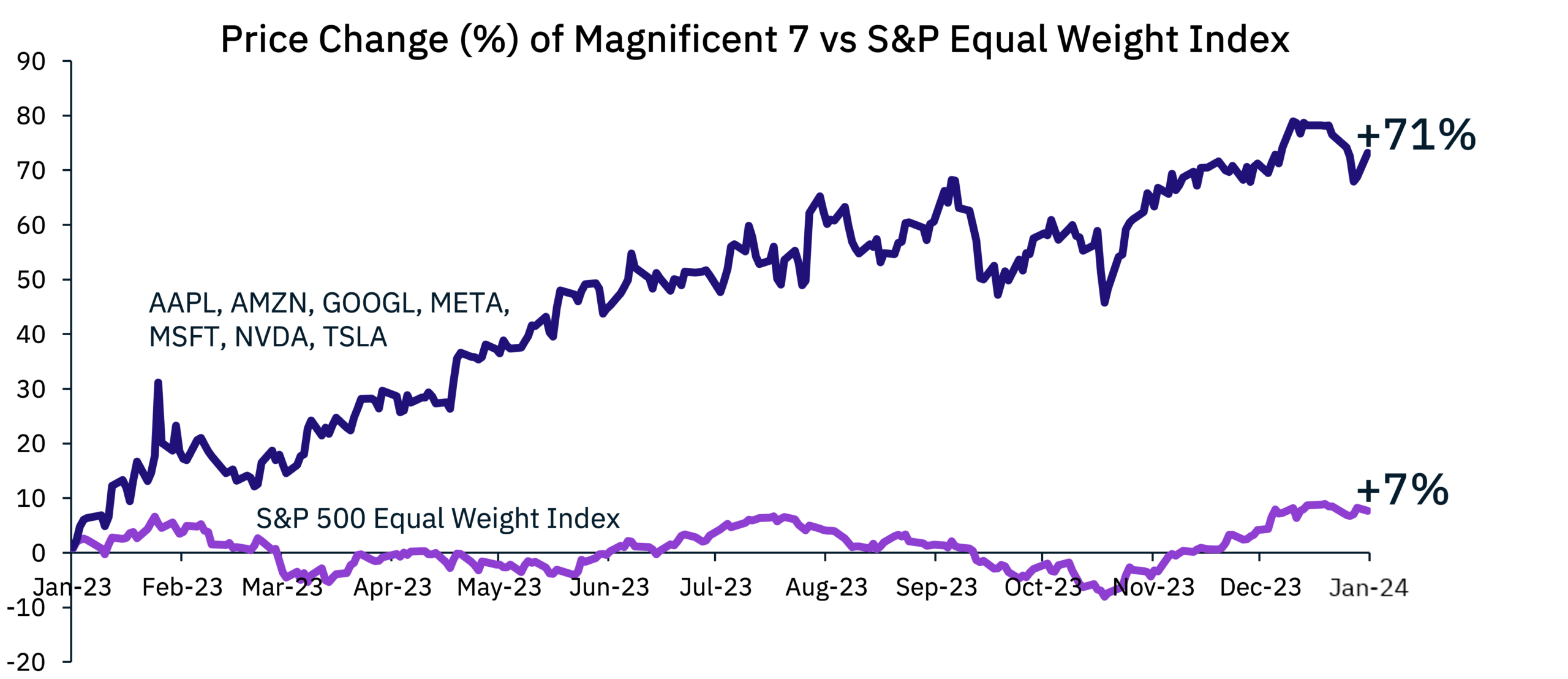

The Magnificent 7 overwhelmingly accounted for the stock market’s 2023 results. Mag7 stocks were up 71%, while the remaining 493 were up only 6%. Today, the Mag7’s aggregate market cap of $11.9 trillion represents 30% of the S&P 500. When you remove market cap weighting from the index calculations, the S&P 500 was up only 7%. Without the Mag7, the stock market has barely beaten the current 5% risk-free rate.

——————

Let’s stop talking about 2023 and focus on what’s ahead – when will the good times return? There’s no crystal ball to determine when the prime exit window will come back, but we do have 30 years of data we can look back on, with some stunning results.

In a show of remarkable consistency, US tech VC-backed exits have peaked every 7 years since the dawn of the modern tech industry. Are we saying we can absolutely predict the next peak? No, but it is reasonable to believe that our next peak will come around 2028.

So, what can entrepreneurs and investors do now? Simple: start preparing.

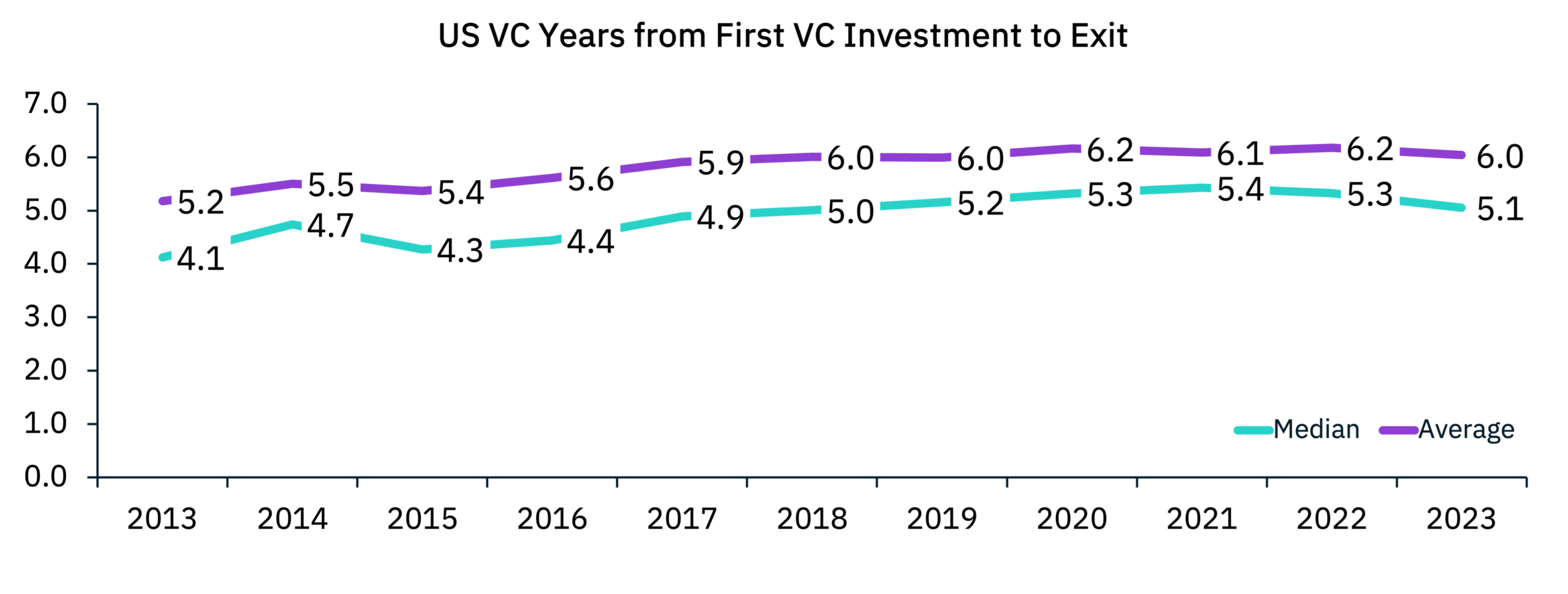

The average amount of time from a company’s first VC investment to exit has stayed pretty consistent at 5-6 years. We believe this means companies raising Series A or Series B rounds right now could be best positioned to time the next big wave. As we’ve seen over and over again in our 20+ years as growth tech investment bankers, fortunes are made based on the groundwork laid in down markets.

As M&A specialists, we’re not going to sit on our hands until 2028. At Bowen, we’ve proven to not just survive, but thrive in difficult markets.