News

News

FTFL - To B, or not to B, That Is the Question

This article appeared in our May 2026 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

We have been at this growth tech banking business for a while now, and spotting trends built on 25 years of scaffolding is one of our favorite things to do.

The financial definition of a Series B has changed dramatically over the years, but the punchline here is “The Series B Decision.”

Many of our prospective clients come to us at this Series B inflection point. The majority of the time the company has created differentiated IP, nailed its product-market fit, and experienced explosive revenue growth, albeit at a subscale level.

So, what’s not to like? A Series B is a no-brainer, right?

Having had the honor of working with many of the great venture investors, the answer is clearly… it depends. 99% of the time, Series B use of proceeds is to build out go-to-market. And, as much as AI is accelerating coding and software development, the buildout of GTM remains time consuming and expensive. Worse, in our experience, it is extremely difficult to get it right the first time.

As we are fond of saying and advising – the AI era has made it remarkably easy to build a great product, and remarkably difficult to sell it.

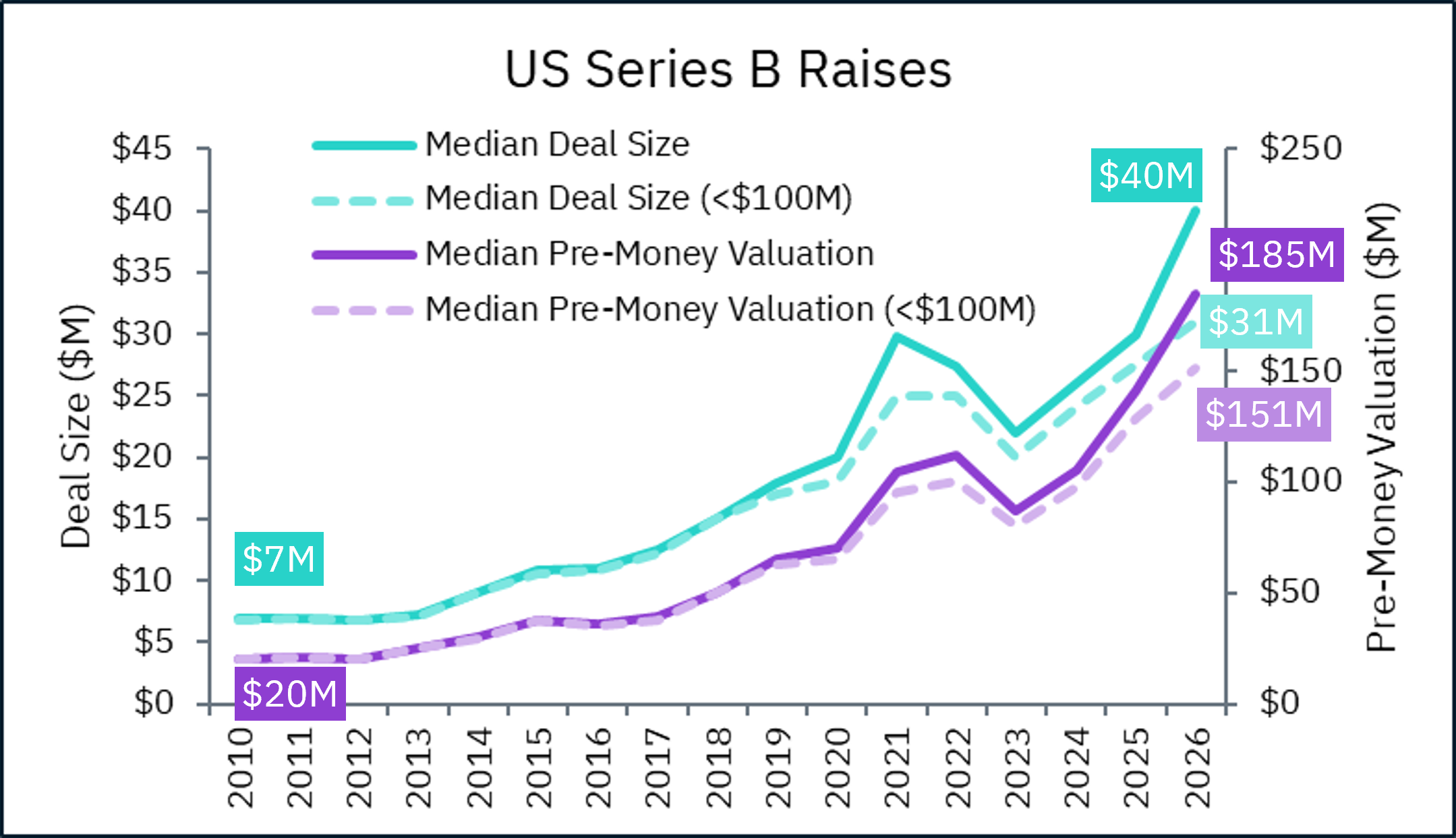

Back to The Decision – let’s dig into the numbers first. My, how things have changed.

A $7M series B at a $20M pre-money valuation seems so quaint now. Deal sizes and valuations rose steadily from 2010 to 2020, then after a post-pandemic bump & correction, a sharp rise fueled by the age of AI. Deal sizes are up 6x and valuations are up 9x since 2010, compared to a 1.5x increase in general prices from inflation. Even if we remove the $100M megarounds that are common among AI unicorns, we still see a 4x increase in deal sizes and 8x increase in valuations.

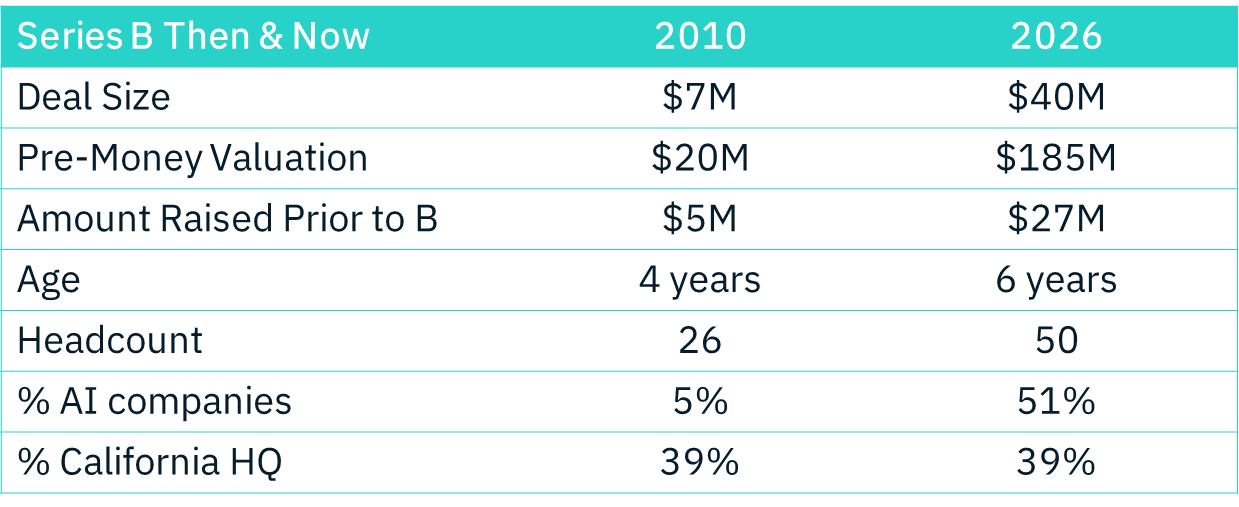

We looked at the profile of a median 2010 Series B company vs. today.

Today’s Series B companies are older and better capitalized going in – more time to build, more prior funding to absorb, more headcount to carry. The other number that jumps off the page: AI companies went from 5% of Series B deals in 2010 to 51% today, a trend we’ve analyzed before. As for California’s grip on venture capital – the Warriors dynasty may be wobbling, but the Golden State’s VC dominance is exactly where it was sixteen years ago, at 39%.

Older, larger companies, doing larger Series B raises at higher valuations – this must dramatically raise the bar on exit expectations, right? Absolutely, which is why this next trend should come as no surprise.

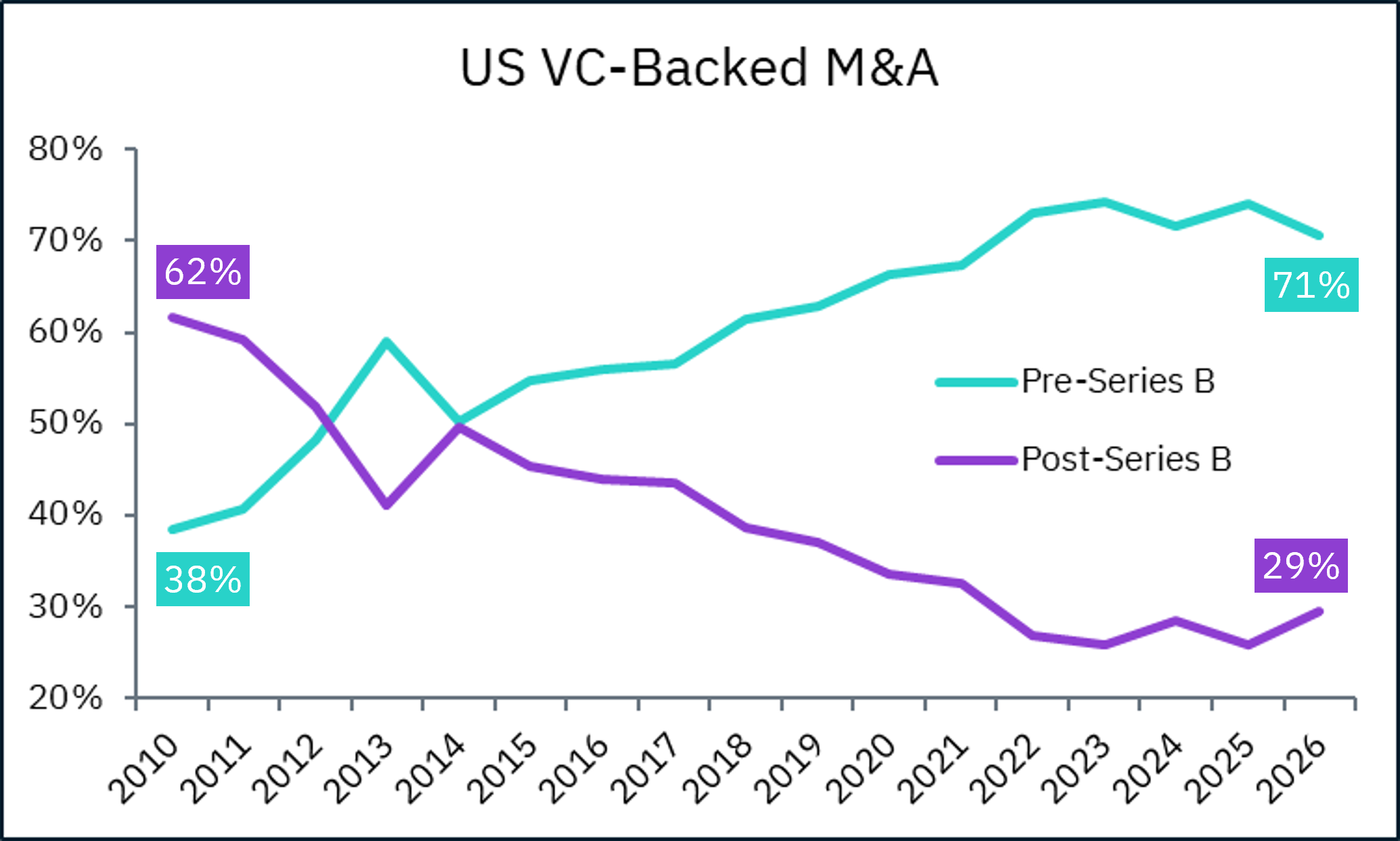

Companies are exiting earlier. In 2010, 62% of VC-backed M&A exits were by companies that raised a Series B or beyond. Today, that number has shrunk to 29%. Meaning fully 71% of VC-backed M&A exits are done by companies that haven’t progressed past a Series A.

Said another way, today there are 2.5x as many companies selling before they reach Series B than after raising a B.

It appears that far more entrepreneurs and investors are seeing “risk” in the risk/reward decision framework when considering a Series B. Let’s just do some back-of-the-envelope math: in 2010, a $7M Series B at $20M pre-money meant that a post-B $100M sale would be a strong outcome. Today, a $40M Series B at $185M pre-money implies a billion-dollar exit is required to achieve similar investor IRR happiness. We can see how that kind of daunting expectation would lead to earlier sale processes – and for more founders, The Series B Decision is becoming an easy one.

Sixteen years ago, LeBron’s Decision wasn’t a retreat – it was a recognition that joining the right team beats forcing a solo run. More founders are taking their talents to South Beach before the Series B math turns a great outcome into a consolation prize.