News

News

FTFL-GE: Conflict as Catalyst: How Geopolitical Disruption Is Building the Market for Energy Intelligence

April 2026 issue of From the Front Lines (Green Edition), Bowen’s dedicated sustainability sector newsletter, spotlighting tech trends and insights in Agriculture, Water and Waste, and Energy.

Energy security includes both independent, continuously available energy sources and a reliable distribution grid to manage energy inputs against demand. Incorporating intermittent and distributed renewable energy sources into the grid requires a new level of grid management and sophistication. Geopolitics is changing the cost vs risk equation of energy generation, accelerating adoption of renewables and therefore the need for flexibility and intelligence in the grid.

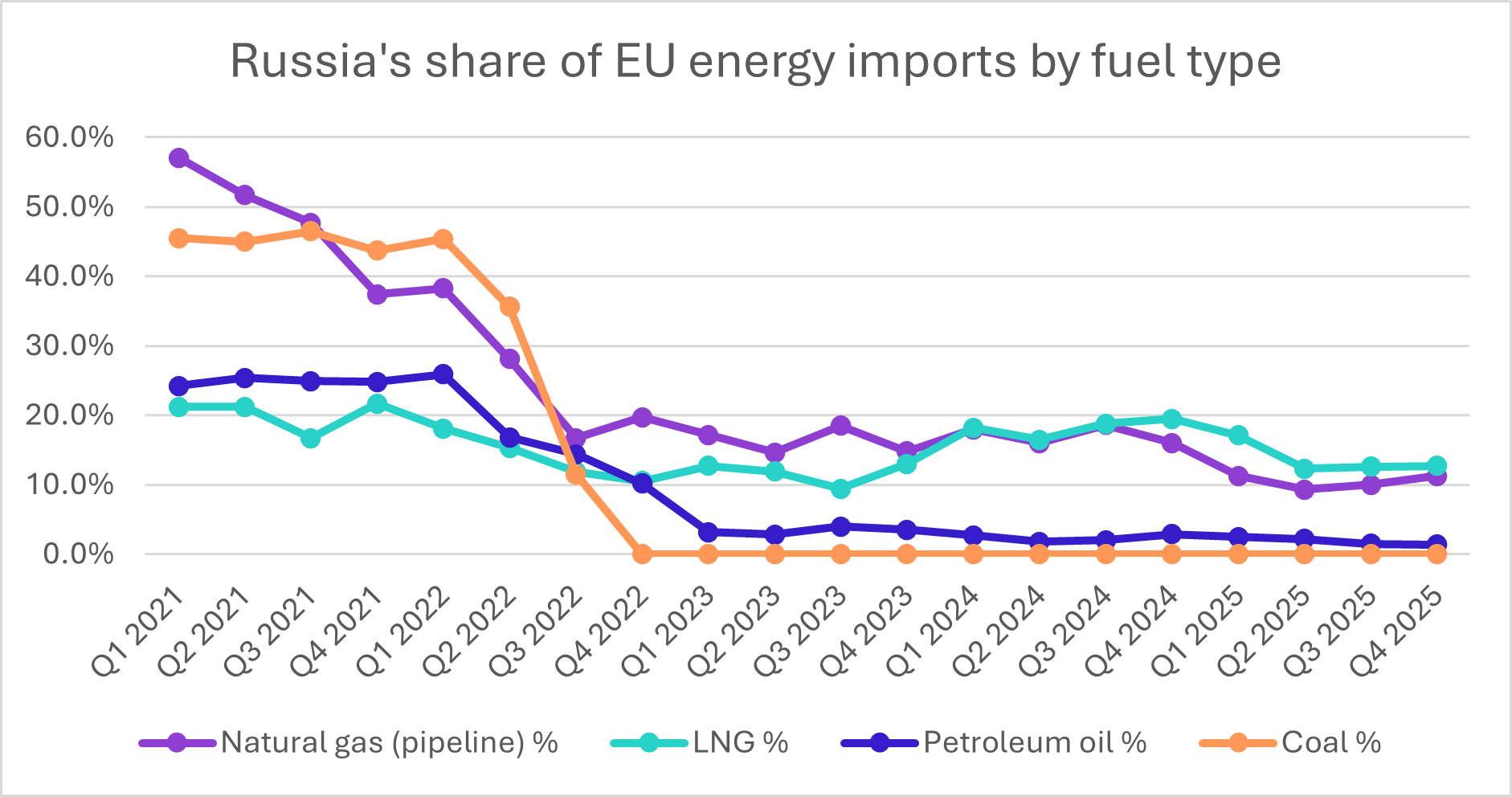

When Russia invaded Ukraine in February 2022, Europe discovered how completely it had outsourced its energy security. Russia supplied 38% of EU natural gas, 26% of its oil, and 45% of its coal. For the countries closest to the conflict, the exposure was existential. Finland, Estonia, and Bulgaria sourced 100% of their gas from Russia. Germany relied on Russia for 65% of its gas imports. The risks had been visible for years; they were largely ignored until they could not be.

The EU’s swift response significantly altered the energy landscape, more so than years of climate policy or energy transition planning. Germany built its first LNG import terminal in nine months. The EU launched REPowerEU within three months of the invasion, targeting a 70 billion cubic meter cut in Russian gas imports within the year. Coal imports were banned by August 2022, crude oil followed in December, and refined petroleum products in February 2023. By the end of 2023, the EU had cut its monthly fossil fuel spend on Russia from €16 billion to roughly €1 billion. A decoupling that experts had called structurally impossible was largely complete in under two years.

LNG was first to fill the gap. US LNG exports to the EU more than doubled in 2022 relative to 2021 and the US grew its share of EU LNG imports from 29% to 53% by 2025. While fast to contract and politically palatable, the required substitutions multiplied supplier relationships, delivery routes, and pricing exposures overnight.

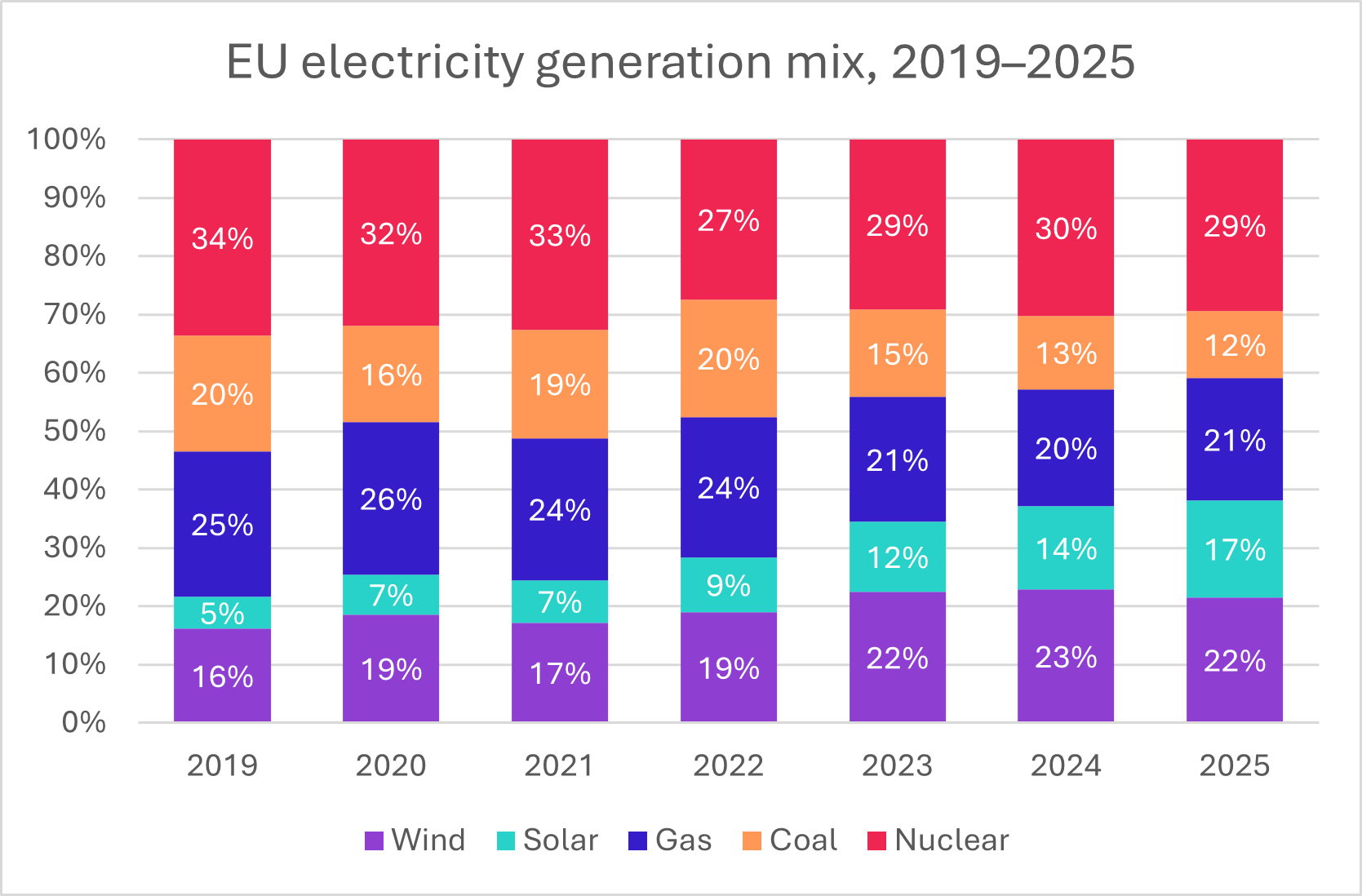

Renewables filled the gap more permanently. Wind and solar grew from 22% of EU electricity in 2019 to roughly 38% by 2025, solar nearly tripled, coal fell 42%, gas fell 16%, and in 2022, renewables outproduced gas for the first time. Integrating 58% more renewable capacity into grids not designed for intermittent generation created its own operational problem: balancing variable supply against industrial demand, in real time, across a fragmented and rapidly changing system. Energy management systems, remote monitoring, and AI-enabled dispatch tools became as operationally critical as the turbines and panels themselves. Unlike the physical build, they could be deployed in months, not years.

Policy that would have taken a decade was accomplished in a quarter; infrastructure requiring years of permitting was built in months. Critically, the strategic imperative arrived precisely as the economic argument was put to bed. Solar and wind crossed grid parity in most European markets during the same period that Russian gas became a liability. The political and investment cases converged at the same moment, resulting in structures likely to last for 20 to 30 years — REPowerEU, revised renewable targets, Baltic grid synchronization, LNG phase-out legislation, and a €45 billion EIB commitment. The infrastructure, operational complexity, and the technological solutions required are likely to last longer than the conflict that spawned them.

Iran Conflict Implications

The Iran conflict is a supply shock with potentially greater global impact. The Strait of Hormuz is a single 33-mile passage through which 20 million barrels of oil and approximately 20% of global LNG trade moved every day. Immediately following the conflict’s start, Brent crude rose 28% in a week, and European gas prices spiked 20% in a single morning.

The countries most exposed — Japan, South Korea, and Australia, which collectively account for the majority of Hormuz-transiting LNG flows — are now confronting the same calculus Europe faced in 2022, with one critical difference: the economic case has already been made. Domestically generated renewable power cannot be sanctioned, blockaded, or priced by a cartel. Unlike Europe in 2022, grid parity is an established fact. The security premium and the cost advantage point in the same direction simultaneously, turning an emergency response into a structural, durable investment rather than cyclical hedging.

In the US, oil prices immediately impact the economy even though it is a net oil producer. Simultaneously, rising energy demand from data centers further stresses infrastructure. The US model of a secure, diverse energy infrastructure will likely include more fossil fuel than Europe, but it’s sure to include local energy generation and storage. Efficiently managing US energy needs will require new software, sensors, and, increasingly, AI-enabled decision infrastructure to link everything together.

Conclusions

Even when oil prices inevitably go back down, supply risk due to geopolitics has been highlighted. Every electrical grid has to actively manage increasingly distributed and renewable energy generation, which is exactly the problem that AI-native platforms are built to solve: optimizing across multiple sources, automating dispatch decisions, and flagging anomalies before they become outages. US industrial giants serving these markets are increasingly leveraging M&A to add new capabilities to their existing platforms. This has created a seller’s market (our recent energy tech industry report has the details – reach out for a copy). For investors and acquirers, the asset class that benefits most from geopolitical volatility may not be the commodity itself, but the intelligence layer built on top of it.

Bowen, as a global investment bank, works with the companies and investors positioned at the center of that reorganization. Whether the opportunity is in grid infrastructure, renewable development, or storage, we bring the transaction expertise and sector depth to help our clients move with conviction. The map is being redrawn. We help you find your place on it.

From the Front Lines by :