News

News

FTFL - Trend vs. Truth

This article appeared in our January 2026 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

As we kick off 2026, the second half of the 2020s and the eve of a quarter century at Bowen, we find ourselves filled with nostalgia. We pine for the “good ol’ days of growth tech” when everyone knew what a Series A financing actually meant, private capital didn’t load, reload and overload a handful of companies, and entrepreneurs aspired to build a great public company. What hopeless romantics we are! Over the course of 35 FTFLs we have tried to wow you with facts, figures and statistics, and shine a spotlight on growth tech trends. Funny thing about trends, they eventually become norms…

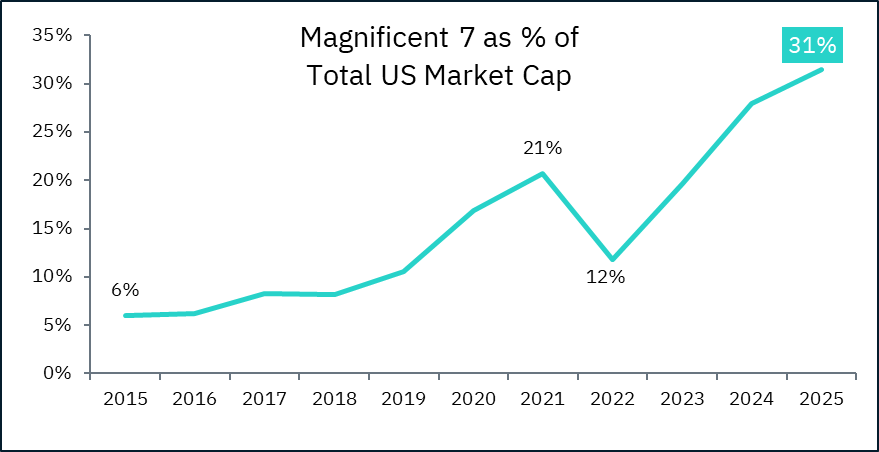

First we look at market concentration over time, and of course that should start with the Magnificent 7, which now represents 31% of total US market cap.

“Magnificent 7” wasn’t a thing a few years ago, so the sharp increase in the graph doesn’t mean much, but surely if we substitute other companies, there must have been a strong concentration at the top, right?

Nope. This is truly a new situation.

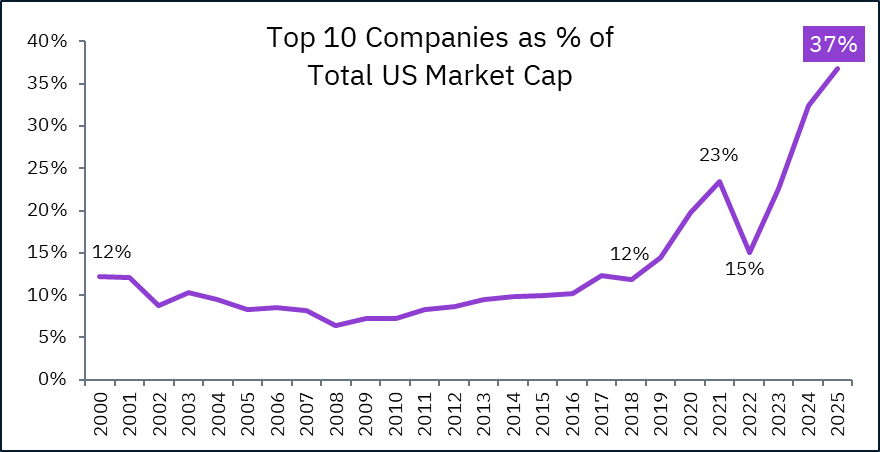

From 2000 to 2018, the top 10 companies by market cap never exceeded 12% of total US market cap. Today, the top 10 account for 37%.

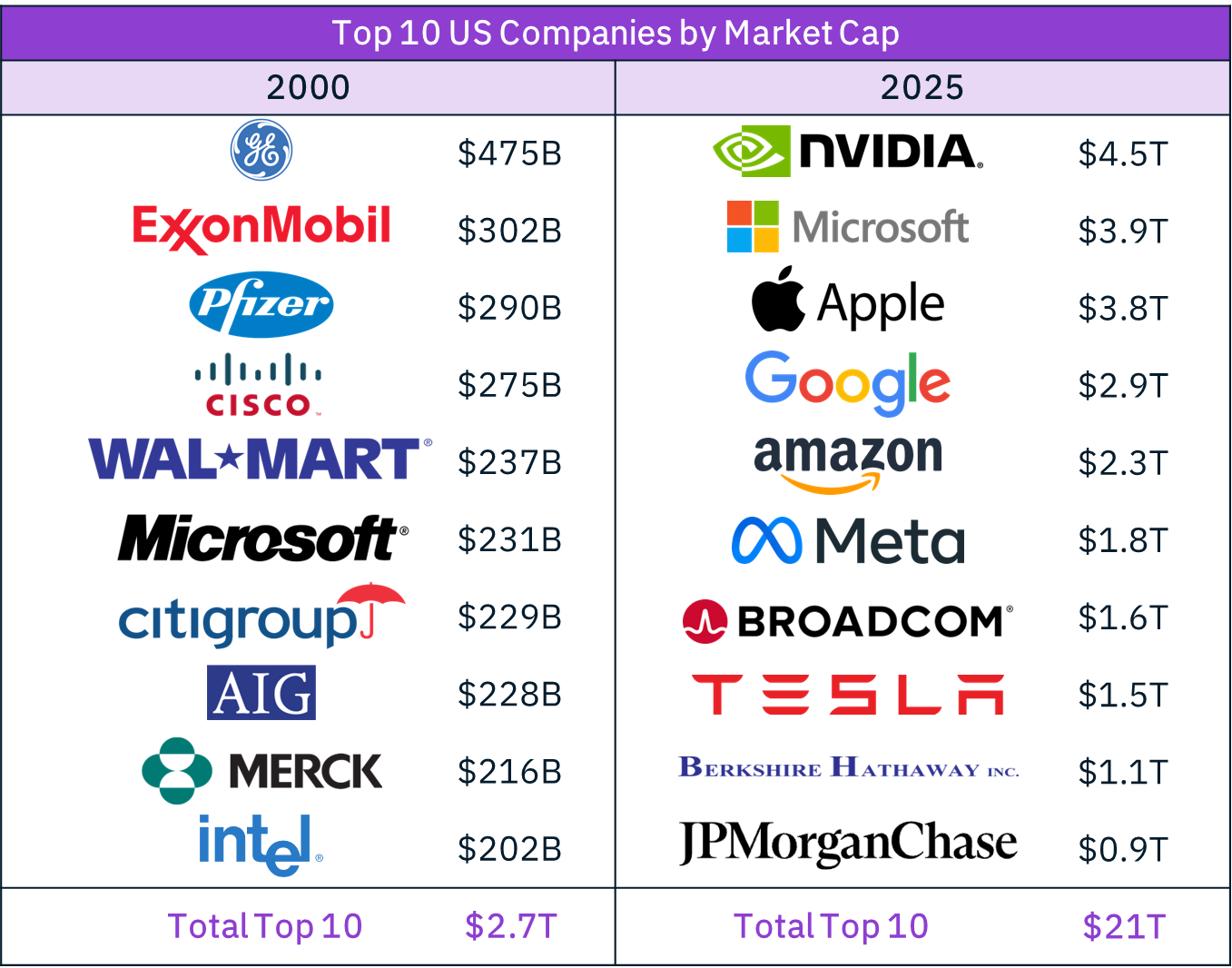

Let’s compare the top 10 in different eras. A lot more industry diversity back then.

A couple notable stats – today’s top 10 in aggregate is greater than US total market cap in 2000, and NVIDIA at its October $5 trillion peak was nearly 2x the 2000 top 10 combined.

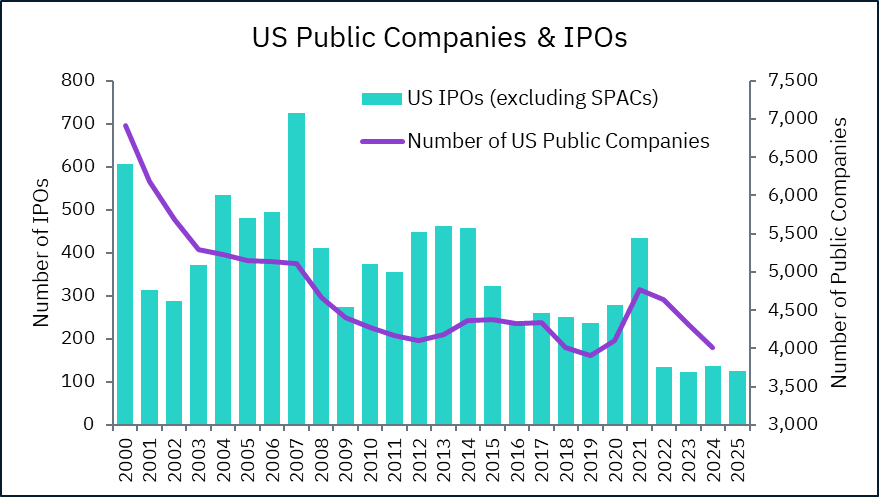

Next we look at the long-declining universe of public companies and IPOs.

Per World Bank data, US public company count has dropped 42% from 6,917 in 2000 to 4,010 in 2024. Meanwhile, the number of annual IPOs has dropped by more than half, from an average of 450 during the first decade of this century to 221 over the last ten years, and dropped by more than 70% to 130 over the last 4 years.

We know, we know, we’ve talked about this a lot in our FTFLs (and as recently as last month!), but we think it’s worth repeating. Strong and diverse public markets are critical to the broader financial ecosystem – from 401k’s to shareholder liquidity to basic valuation metrics. (And of course, more buyers for our sellside clients.)

This data got us wondering, what happens to a newly public company over the long term? From the peak year of 725 IPOs in 2007 from the chart above:

- 34% are still public today

- 54% have been acquired or gone private

- 12% have gone out of business

Now let’s analyze the private markets in a few dimensions

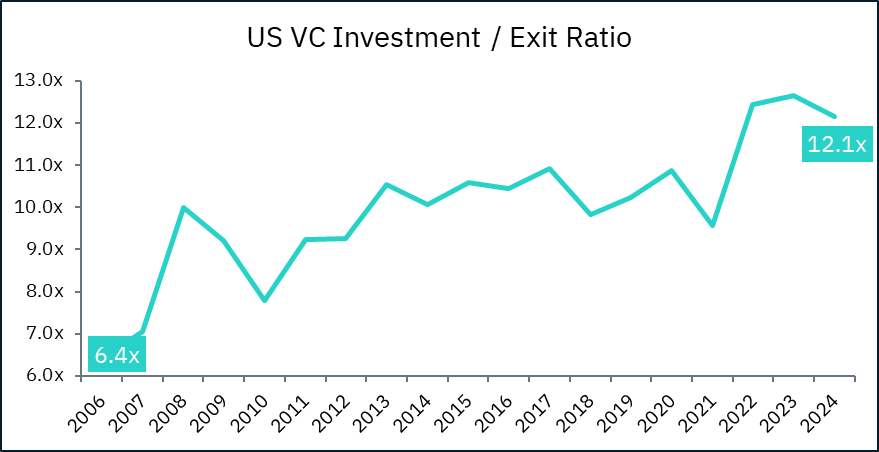

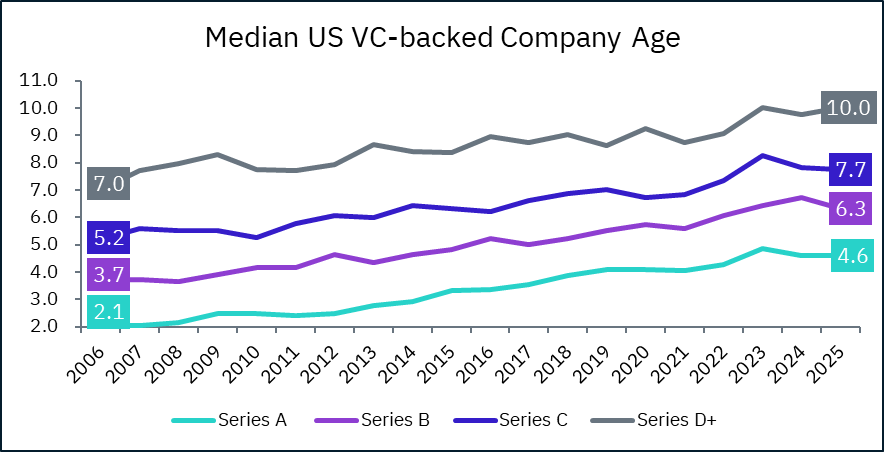

The first graph tracks the number of VC investments vs. the number of exits over time. This ratio has nearly doubled from 6.4x in 2006 to 12.1x today – creating a backlog across all classes, not just unicorns. At the same time, private companies are getting older at every funding milestone, with the median age at each round increasing by 2.5+ years. This stretches the private-market lifecycle at every stage – long before any exit is in sight.

(And for those of you embarrassed you don’t know what a Series A means anymore, don’t feel bad – over the past 10 years, the median Series A raise has more than tripled, from $4.1 million to $14 million. Today’s Series A is closer to what a Series C looked like in 2015.)

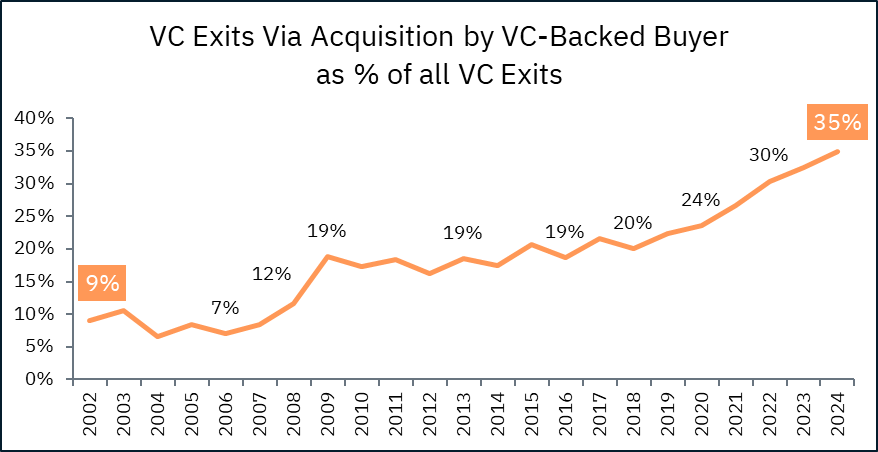

So what happens when a shrinking public market meets a growing private backlog?

VC-backed companies increasingly become the buyers of other VC-backed companies. Over the past two decades, private-to-private M&A has grown from a niche outcome (<10%) to a meaningful share (35%) of all venture exits.

Combine this dynamic with the growth of VC secondaries, and we see private capital recycling internally rather than waiting for traditional exit markets to return.

Three years into our FTFL journey, we’ve written about changes in market concentration, public markets and VC liquidity many times, with the goal of shining a light on the magnitude of these changes. After years of highlighting these anomalies, it’s now clear they aren’t anomalies at all – these trends are foundational and here to stay.

Trend becomes truth.