News

News

FTFL-GE: Ag Tech Year in Review: Any Green Shoots Apparent?

January 2026 issue of From the Front Lines (Green Edition), Bowen’s dedicated sustainability sector newsletter, spotlighting tech trends and insights in Agriculture, Water and Waste, and Energy.

Happy New Year! It’s time to take a look back at 2025 and see what the trends tell us for 2026. We don’t have all the Q4 2025 data yet, but what we have tells an interesting story. It is no secret that 2025 was a tough year for US agriculture, especially row crops. Tariffs and retaliation shut down large parts of the crop export market, particularly soybeans, and input prices remained stubbornly high, driving many farmers into the red. Market conditions were not conducive to significant new infrastructure investments nor experimentation with new technologies and techniques.

The slowdown was not helpful in alleviating the lack of liquidity that has plagued Ag Tech venture capital. Relative to some other sectors, it has taken more time to build VC-backed companies to the scale required for attractive exits. These dynamics have caused many Ag Tech venture investors to exit the market, reduce their commitments, or move to later stage investing, causing a downturn in investment.

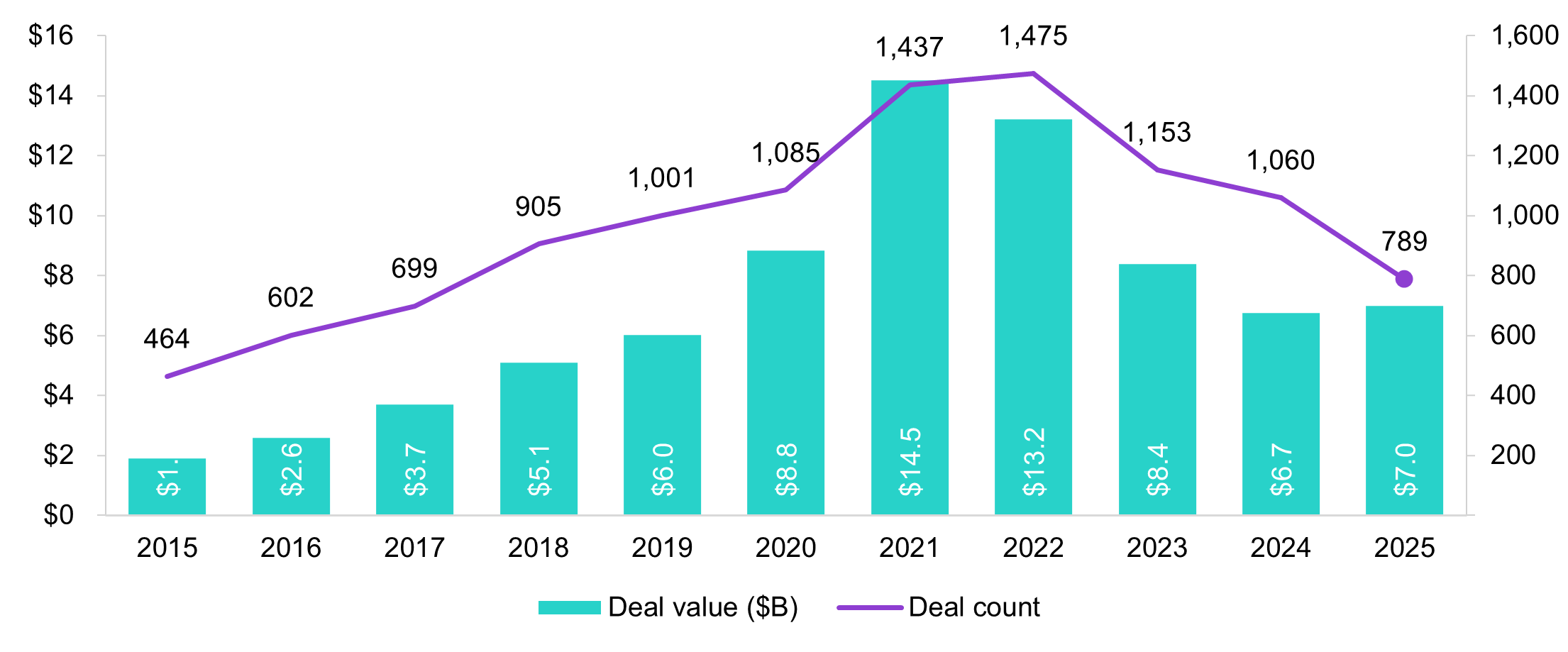

Figure 1 is a look at recent investment activity across all Ag Tech segments, including the full year 2025. Annual deal count continued to drop but deal value actually increased, indicating that investment is moving to later stage opportunities.

Figure 1 – Ag Tech VC Deal Activity (Source: PitchBook)

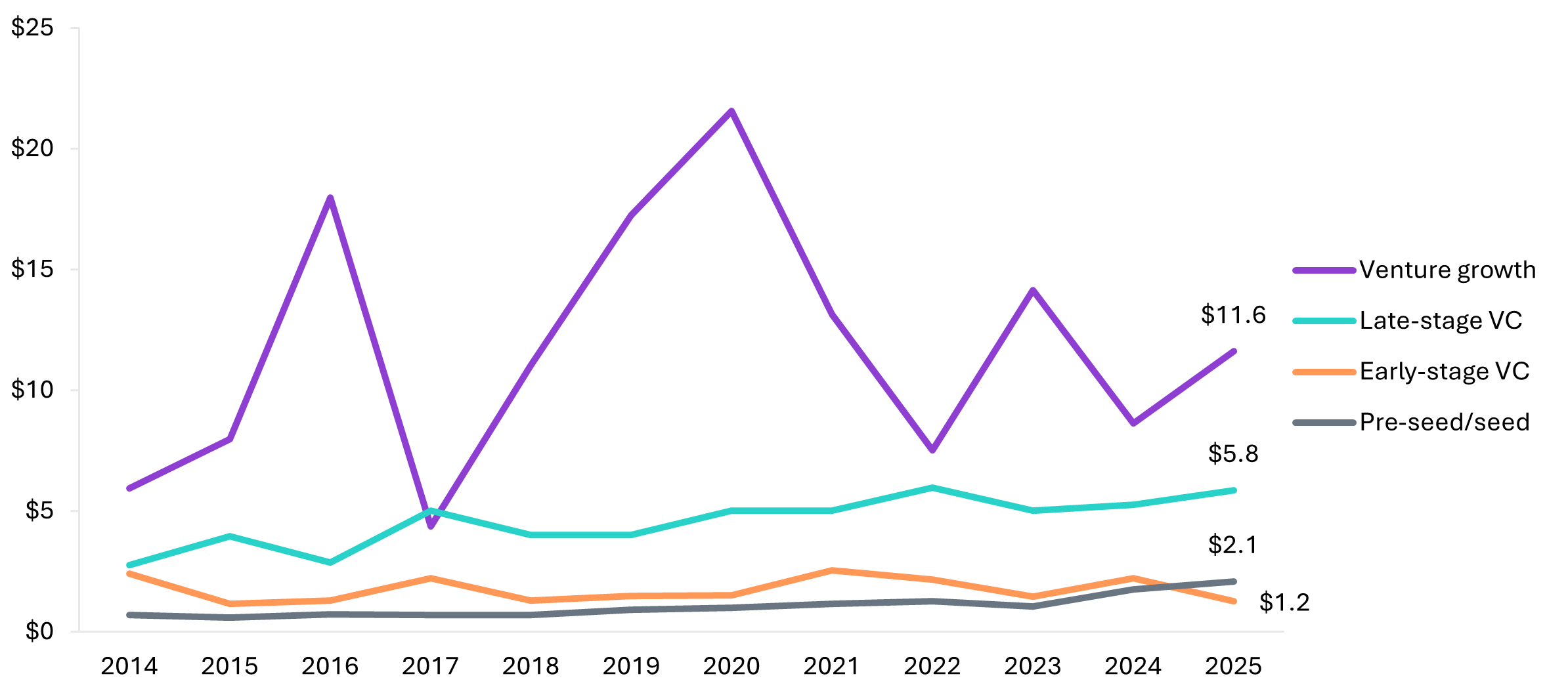

Figure 2, which has data through Q3, supports that view. Round sizes for late-stage and growth investments rose in 2025, while early-stage rounds have shrunk.

Figure 2 – Median Ag Tech VC Deal Value ($M) by Stage (Source: PitchBook)

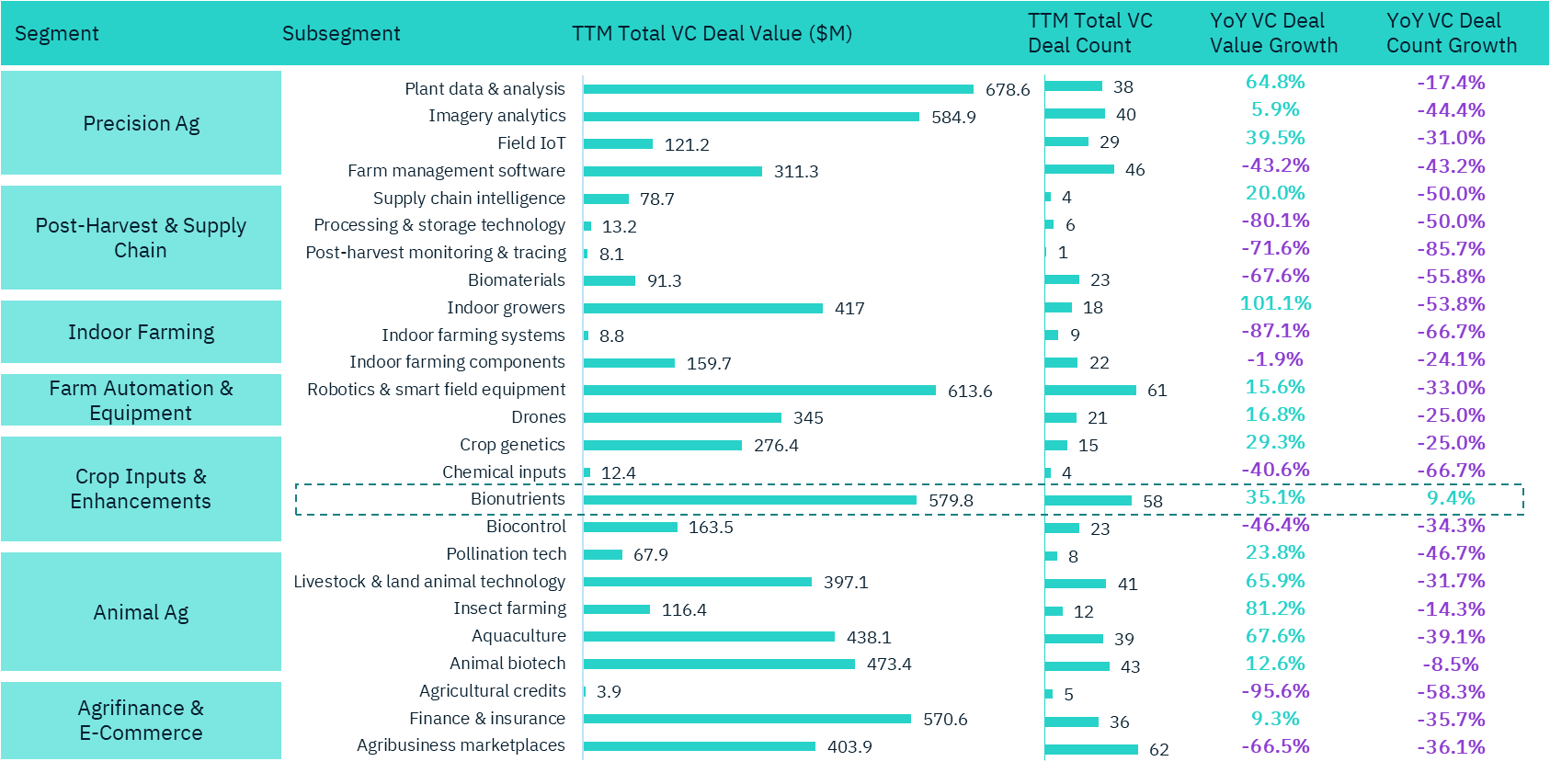

Where are the green shoots? Looking at Figure 3, again showing data through Q3, one stands out.

Figure 3 – Ag Tech Heatmap by Subsegment (Source: PitchBook)

Bionutrients is the one category where both deal volume and deal value have increased. We think that it is an indicator that the sector is coming of age. Ultimately, successful companies improve profitability for the farmer. We’re seeing more biologics companies – often in conjunction with precision farming soil and crop analytics – demonstrate consistently strong economic benefits. That bodes well for the sector, although in classic venture capital fashion, it is highly likely that too much money has gone into too many companies. Consolidation is coming, and there will be companies that generate meaningful value, but not enough to justify the investment they have received. Where do we stand on that score and what does it imply for M&A in 2026?

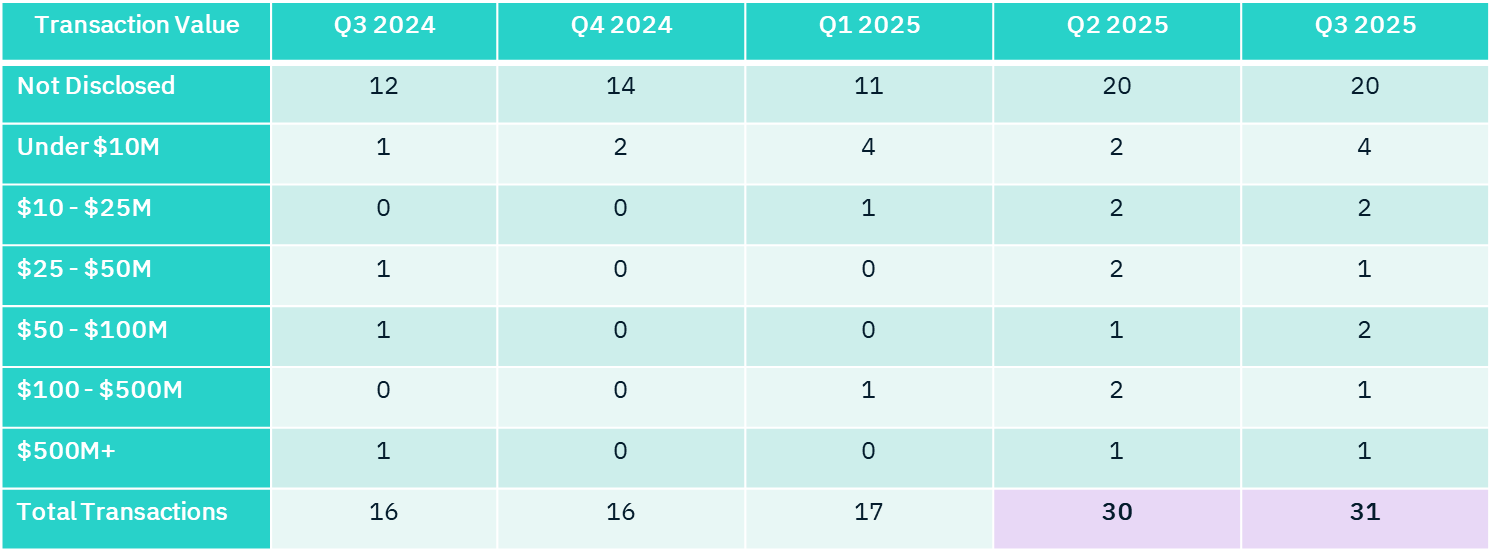

Figure 4 – M&A Deal Count by Deal Size (Source: FactSet)

Deal count picked up in 2025 after a slow start, with Q3 reaching 31 deals, up 82% from Q1. We note that most of the deal values were “not disclosed”, so we should be careful to draw firm conclusions. However, the majority of deals with disclosed values were under $25 million, leading us to suspect that most of the undisclosed numbers were also of modest size.

We see 2026 as an active year for Ag Tech M&A as market conditions stabilize. We believe the worst of the damage from tariffs and broader uncertainty has likely passed. Farming markets should stabilize around a “new normal,” and high-quality companies – those that are profitable and of sufficient scale – should trade well.

That said, as in every venture cycle, more companies have been funded than the market can rationally absorb, and many have raised more capital than their exit valuations will ultimately support. As a result, management teams and investors face three paths:

- Cut costs to reach profitability and wait for valuations to improve, where possible

- Pursue a full sale at prevailing market multiples

- Consolidate with complementary companies to achieve scale and profitability

Not every company has the growth potential or balance sheet flexibility for the first option, and raising additional capital would potentially be highly dilutive. A full sale at compressed multiples can be painful, but for some, it will be the most rational choice.

Consolidation is likely to be most attractive for companies that deliver clear economic value to their customers. While complex cap tables and integration challenges add friction, achieving scale and category relevance materially improves the odds of a desirable outcome. Consolidation and portfolio rationalization are necessary to restore balance to the market. The data suggests that process is beginning – signs of sprouts for Ag Tech.

From the Front Lines by :