News

News

FTFL-GE: Carbon Credit Market Check-In

May 2025 issue of From the Front Lines (Green Edition), Bowen’s dedicated sustainability sector newsletter, spotlighting tech trends and insights in Agriculture, Water and Waste, and Energy.

At the beginning of the year, we opined that after a down year in 2023 and flat 2024, the carbon credit market would stabilize and begin to turn upward in 2025, particularly later in the year. We’ve seen a fair number of interesting headlines in the space recently, so we thought now would be a good time to check in and see how things are turning out.

Higher standards are driving up carbon credit quality, leading to a balance, and possibly near-term shortfall, in availability, potentially driving prices higher

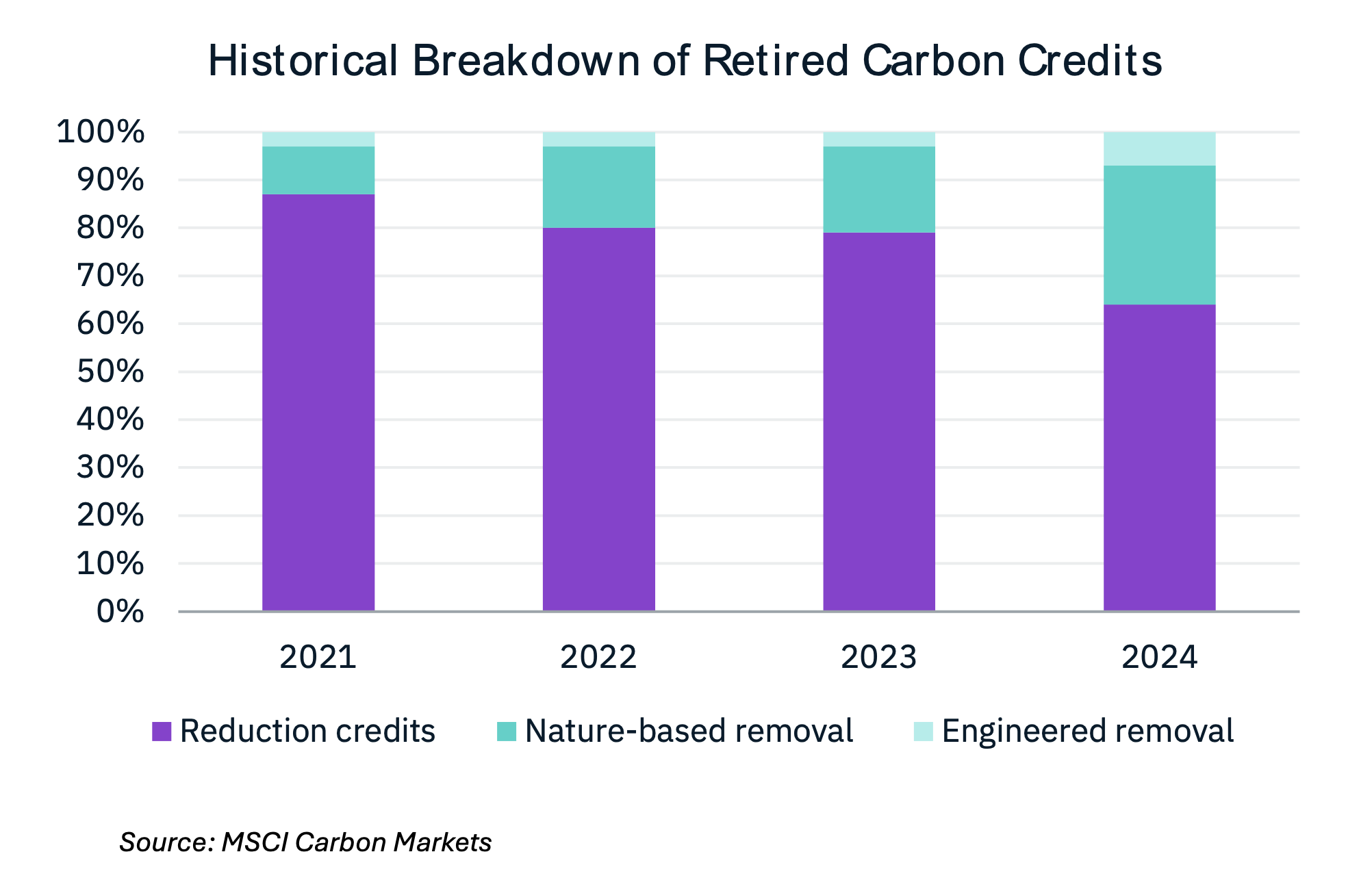

According to data from carbon-credit rating platform Sylvera, Q1 2025 represented a dramatic realignment of supply and demand in the carbon credit market. Fewer but higher-quality credits are being issued. A seeming oversupply of credits issued vs those retired has disappeared, with the number of issuances and retirements in Q1 nearly equivalent at about 55 million credits. Contrast that with the first quarter of 2024 when 83 million credits were issued and about 55 million retired. Sylvera believes that 2025 could be the first year in which retirements exceed issuances.

Shifts in credit type support the “move to quality” thesis. Carbon removal credits are considered higher quality than emission reduction credits because they represent measurable, permanent removal of CO₂ from the atmosphere. As a result, they tend to trade at higher prices. In 2024, carbon removal credits jumped to become about a third of the market by dollar value, after years of being 20% or less of carbon credit retirements.

Standards organizations are raising the quality bar for carbon offsets, and a lot more companies have set voluntary market compliance targets

- The Integrity Council for the Voluntary Carbon Market (ICVCM) has issued its Core Carbon Principles and is assessing whether carbon crediting programs meet its standards. So far, six programs have been approved, with another 6 in review.

- ICVCM works closely with the ICAO (the UN’s International Civil Aviation Organization), which has created the CORSIA scheme to require airlines to purchase carbon offsets to their emissions. CORSIA sets its own credit qualification standards and its selections are closely watched among voluntary carbon market participants. CORSIA roiled the credit market last fall with some strict standards for clean cookstoves, but providers have adapted to the new requirements, and the market has recovered.

Whether it is a result of increased standardization, less time to hit 2030 targets, or other factors, more companies are setting carbon reduction targets. The Science-Based Targets Initiative (SBTi) is a non-profit organization setting standards for corporations to measure and reduce their emissions. The number of companies with SBTi-approved targets grew by 65% in 2024 to 2,732 companies.

Compliance requirements are kicking in, with Europe leading the way

- Regulatory requirements are starting to drive the carbon markets. CORSIA has been voluntary up to now, but its requirements become mandatory in 2027 and increase each year.

- The preliminary rules for trading carbon credits under the Paris agreement have been negotiated.

- The EU Emissions Trading System (ETS) is a cap-and-trade system in which allowances must be purchased for emissions that exceed an assigned target. The program started in 2005, but new industries are being added and free allowances are gradually being phased out. Allowances are a form of credit that funds green projects in Europe and can be traded as a derivative.

- The EU ETS is complemented by the Carbon Border Adjustment Mechanism (CBAM), which is essentially a tariff on goods in certain industries that are manufactured in countries with more lax emissions standards. CBAM takes full effect in 2026.

- While the US federal government is pulling back from climate subsidies and regulation, individual states like California, or groups of states, like the 11 northeastern states in the Regional Greenhouse Gas Initiative (RGGI), which is structured similarly to the EU ETS, are filling the gap left by the federal government.

The takeaway

We’ve focused on what’s happening now rather than projections, but MSCI, a prominent research firm, believes that the carbon credit market in 2030 will be at least $7 billion, five times 2024’s number, and could be as high as $35 billion.

2025 is still a transition year in the carbon trading space, but a lot of things are going right. We think this is a good time to develop and execute a strategy to monetize carbon reduction in agriculture, energy, and manufacturing. Fluctuations in carbon credit pricing add risk to capital-intensive business models completely dependent on carbon credit sales. However, we see an increasing number of companies selling products and services with carbon credits as an ancillary benefit. We believe that these companies will be extremely attractive targets as more buyers and investors enter the space.

What We’re Reading

From the Front Lines by :

Bob Fleming

Managing Director