News

News

FTFL - Exits Down, Stocks Up?

This article appeared in our January 2025 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

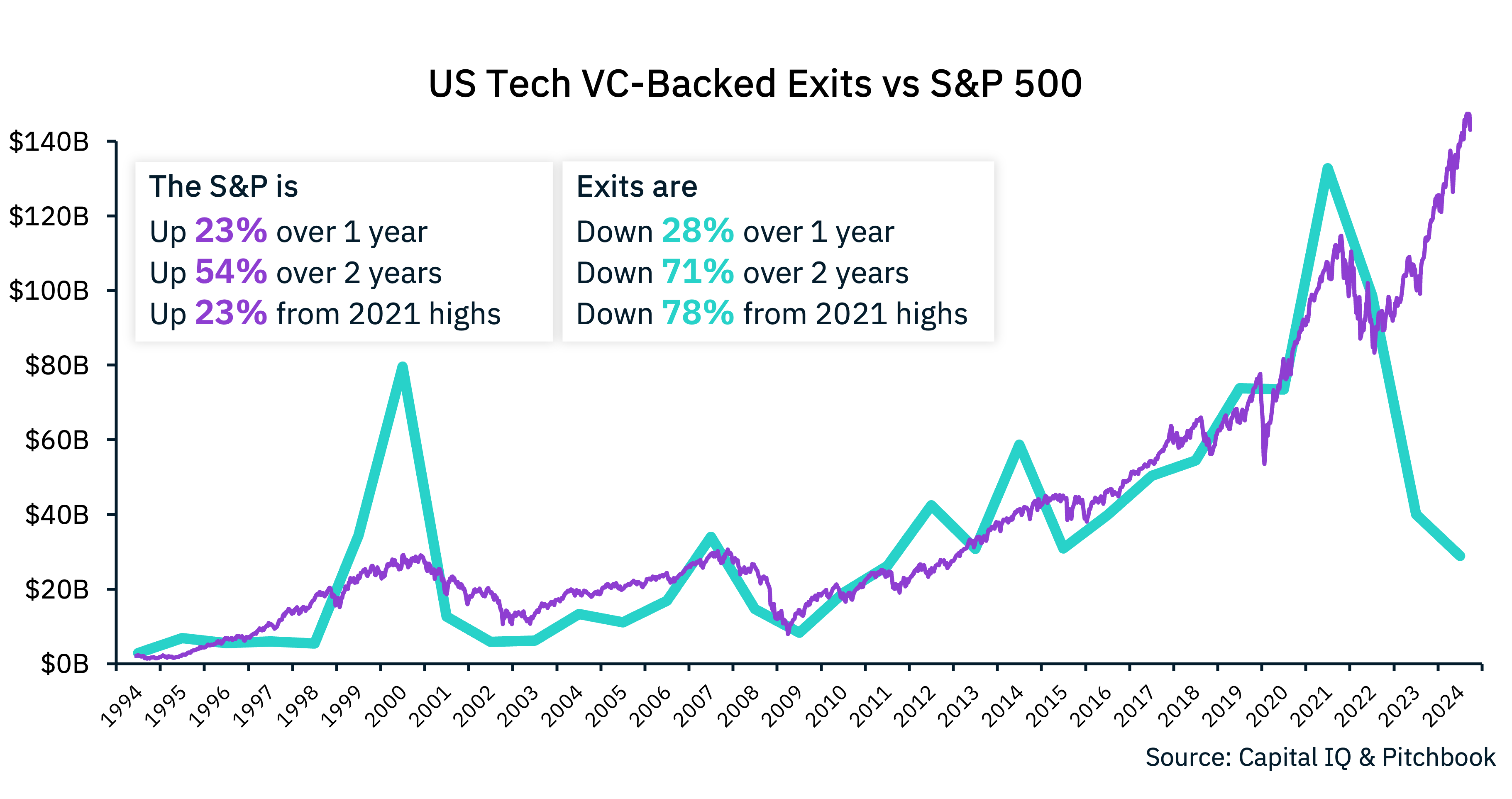

Over the course of 2024, we repeatedly wrote about the VC-backed exit environment. As a growth tech investment bank, we hope you can forgive us for over-rotating on the topic. In FTFL #13 published in January 2024, we tracked US tech VC-backed exits over a 30-year period. This month, we revisit that data with an added wrinkle.

Exit values in 2024 totaled $29 billion, down 28% from 2023 and down 78% from the high in 2021. This happened while the S&P 500 grew 23% year over year, which makes it two years in a row where the stock market is massively up while exits are massively down.

Has this ever happened before? Nope. Never.

For 28 years from 1994 to 2022, the S&P 500 and US tech VC-backed exit values were in near lock-step, peaking and bottoming out at the same times. But it’s been wildly different the past two years. What could possibly explain this?

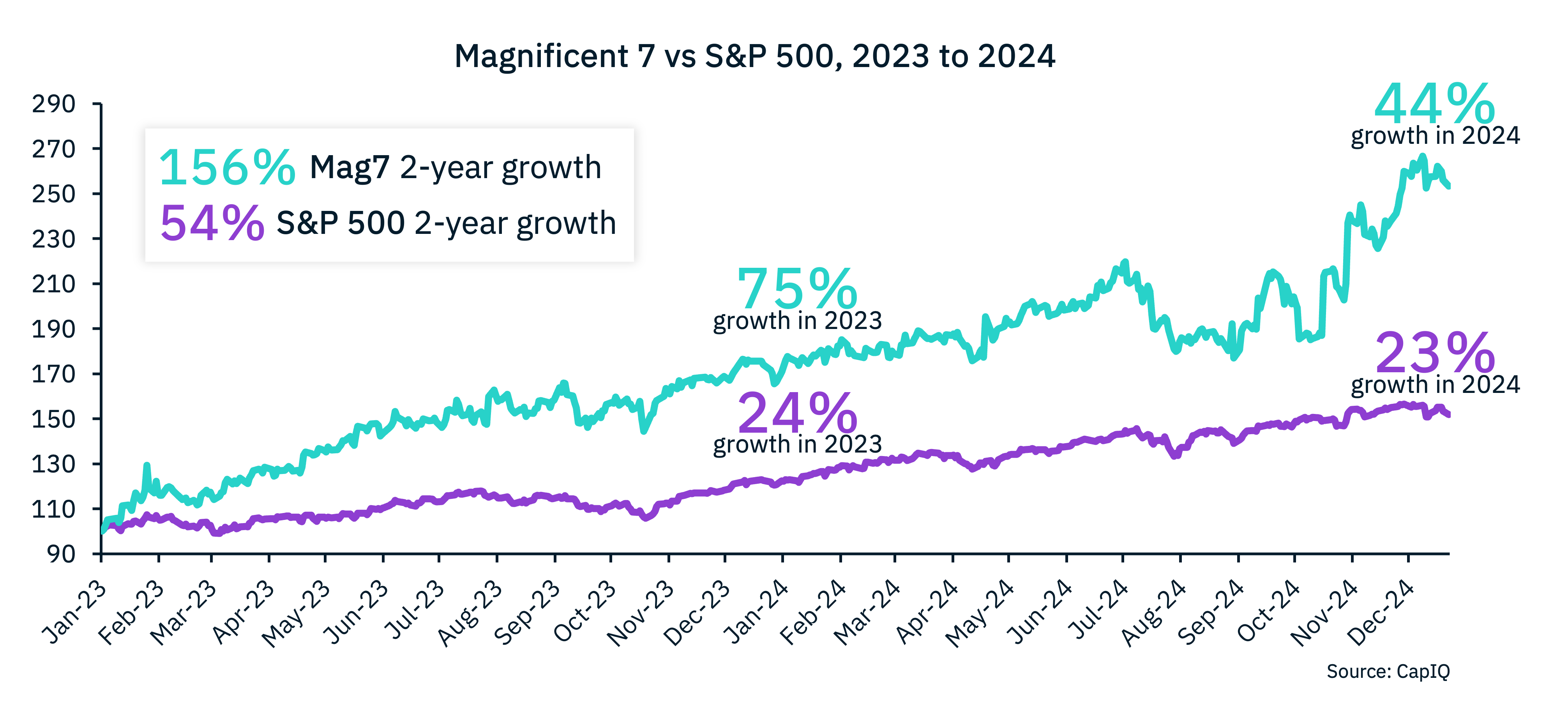

As we showed last year, it must be the Magnificent 7 overinflating the S&P 500’s gains again, right?

Well, not really.

When we remove the Mag 7’s outsized influence by using the S&P 500 Equal Weight Index, we still see two straight years of solid growth. Normalizing for the Mag7, stocks are up 24% over two years while exits are down 71%.

What is going on? How has a 28-year alignment between the public markets and private exits changed so dramatically?

Maybe something bigger is happening here. Perhaps this is not an anomaly, but a fundamental fracture, and the public markets are no longer a leading indicator of VC exits. If that’s the case, we think we know what’s behind it: private equity.

A decade ago, public companies were acquiring nearly 3 times as many VC-backed tech companies as private equity. But as cloud computing and recurring revenue business models became more prevalent in a ZIRP environment, private equity went from tech observers to tech players to tech titans.

Over the past two years, PE and PE-backed companies have been more acquisitive in VC-backed tech than public companies. When public companies were the 3x dominant buyers, it made sense that their market performance would dictate the exit market’s performance. Without that dominance, it appears that the S&P 500 has simply become less important to a VC-backed company’s exit outlook.

And based on the stagnant IPO market, we think it’s increasingly likely that these acquiring PEs will sell their tech portfolios to other PEs – and/or use the secondary market – rather than take them public. Private equity has often been referred to as a club. The club’s best secret? Creating value and not even needing the stock market to do it.

Whether this is a blip or a new reality, it’s clear we need more public tech companies (hi, Unicorns!) and VCs need to clear out their portfolios to keep the liquidity cycle going. On that latter point, we here at Bowen remain steadfastly focused on helping entrepreneurs and VCs (and their LPs) achieve their exit goals.