News

News

Cross-Border, New Order?

This article appeared in our June 2026 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

At Bowen, we are both humbled and proud by the fact that 36% of total transactions have been cross-border over our 24-year history. Navigating the complexities of bringing together buyers and sellers from different countries creates all kinds of challenges – from byzantine regulations to local deal norms to language barriers. We’ve excelled at cross-border because of our experience, our vast network of relationships, and our do-whatever-it-takes commitment to our clients – including the dedication (or idiocy) of doing calls in time zones separated by 13 hours.

For our June FTFL, we posed the question – why do cross-border at all? With 2025’s tariffs and 2026’s wars, how can cross-border with the US possibly thrive when the Scots seem to be our only friends?

Suppositions aside, we wanted to play it straight: Trump administration 2.0 – cross-border M&A tailwind, headwind, or net neutral force?

Before we dive into the data, a few points worth bearing in mind:

1. Only once in US history have we experienced a non-consecutive President serving two terms (can you name the other? We know Abe Simpson can).

2. For the 45th & 47th President, we will examine now nearly 5.5 years of data.

3. For good measure, we will examine investment activity as well.

4. In this FTFL, we focus on international interest in US companies.

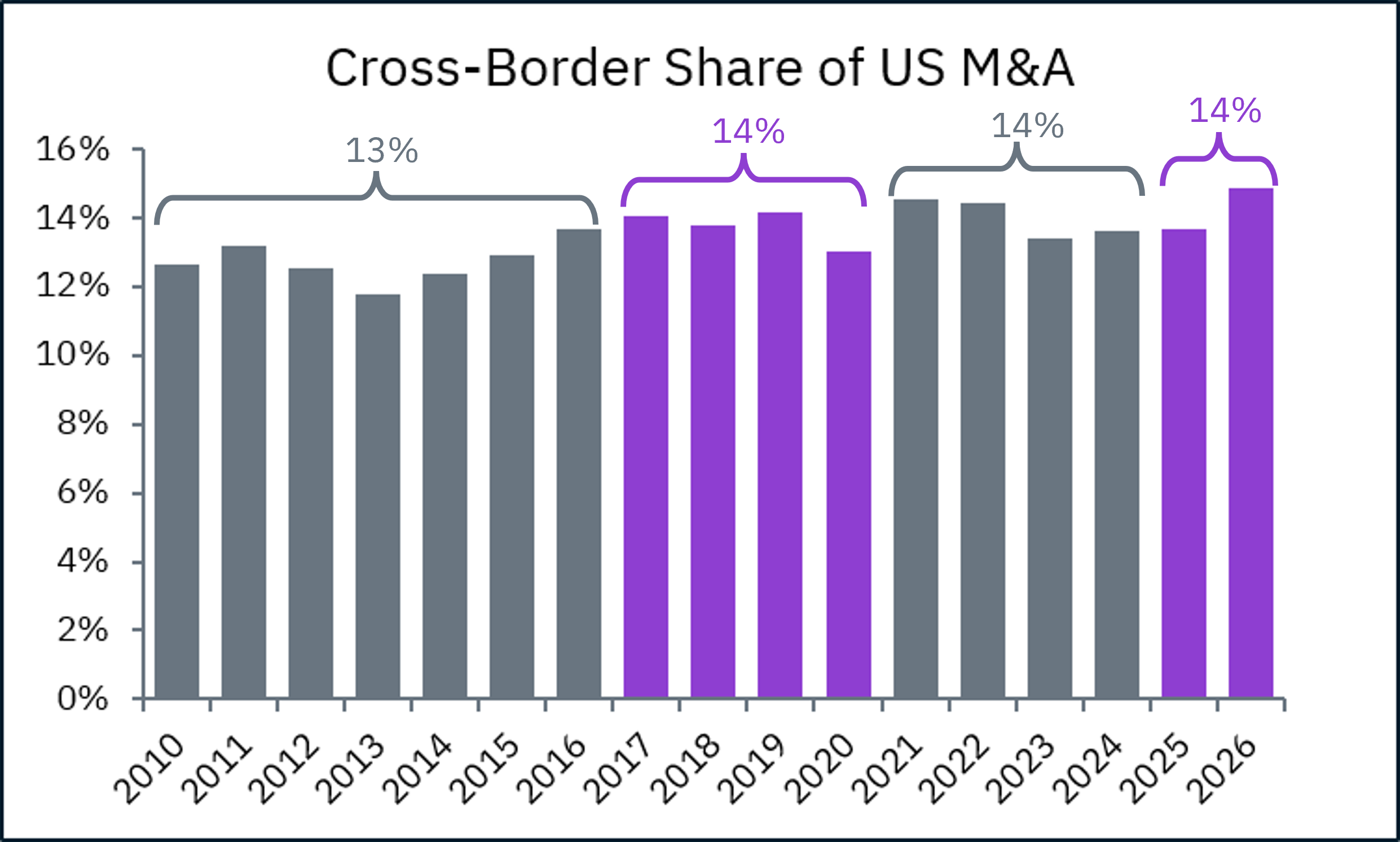

Let’s start with all US M&A targets (for representative scale, there were 16,000+ in 2025) – what percentage have been acquired by non-US buyers over the years, and how has that changed based on who’s in the White House?

We see no effect from Trump’s policies here. If you squint real hard you could make a case that the end of T1.0 scared away some international buyers, who then returned under Biden, but that 2020 dip was almost certainly related to the pandemic.

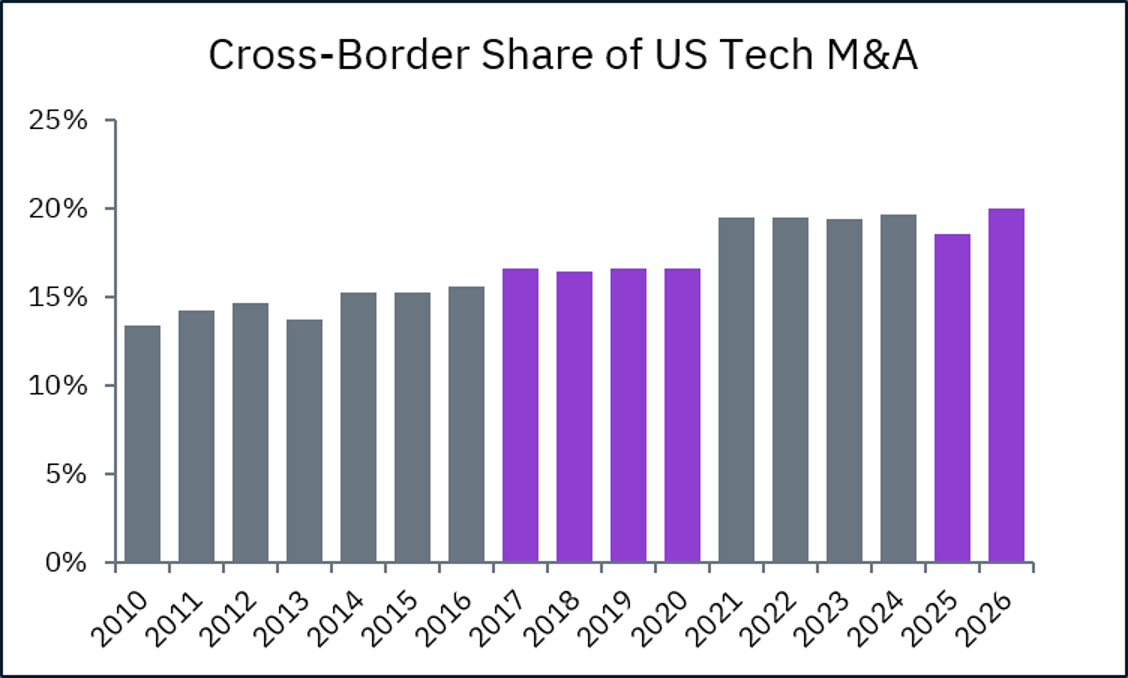

If we look at just Tech M&A, we see a general rise since 2010 and a more pronounced Trump-to-Biden effect, but minimal change in T2.0.

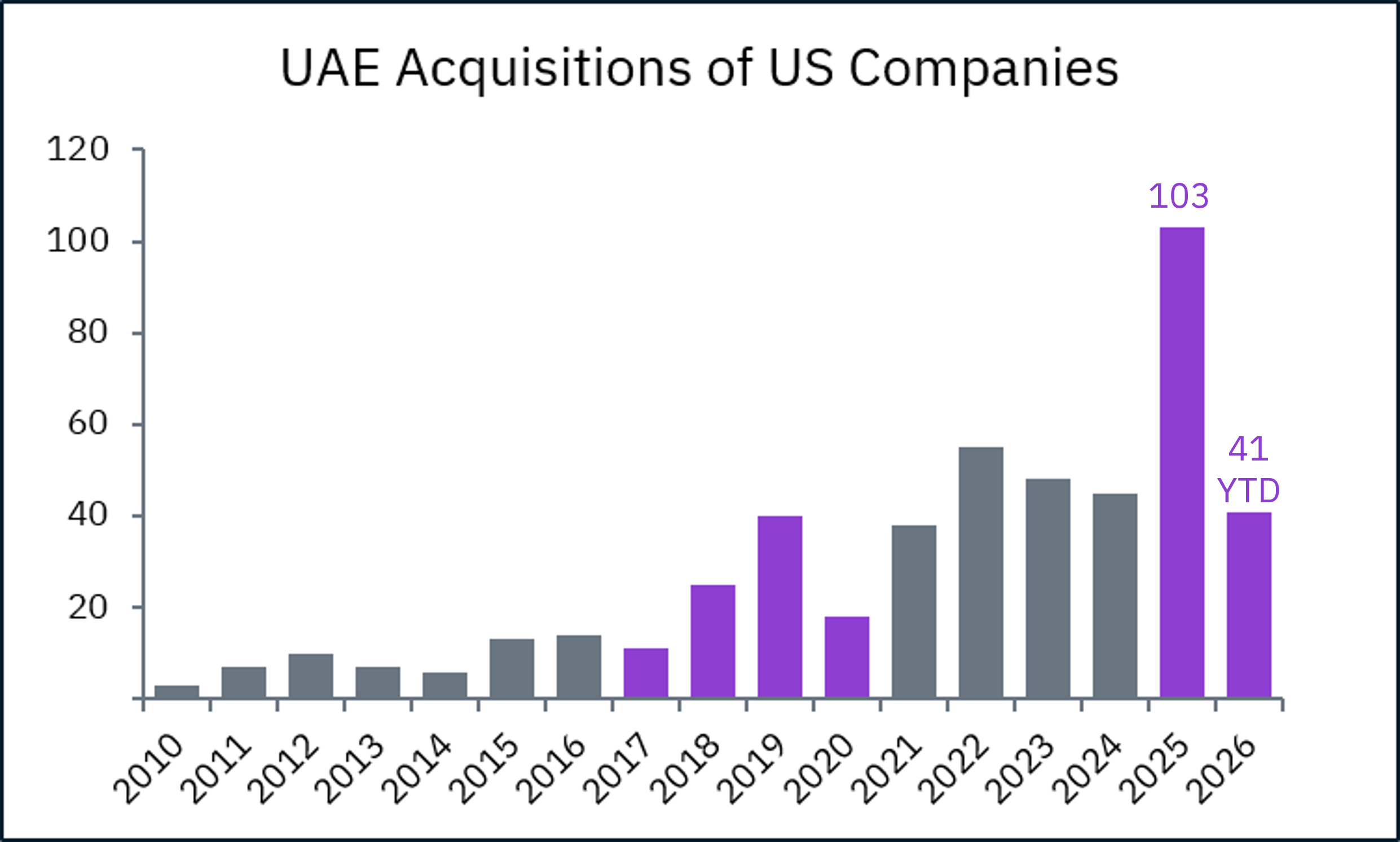

Drilling down, if the administration hasn’t significantly affected overall cross-border M&A, are there any particular countries that stand out? After digging through the country-level data, one acquirer nation stands out.

Acquirers from the United Arab Emirates, particularly the sovereign wealth fund Abu Dhabi Investment Authority (ADIA) have dramatically increased their M&A volume of US companies, starting during T1.0, continuing through the Biden administration, and skyrocketing >11x early in T2.0. Prior to 2017, there were an average of 9 US acquisitions per year by UAE buyers. In 2025 there were 103 such deals. That trend, combined with the Wall Street Journal’s reporting earlier this year, certainly indicates that the pace of UAE-sourced deal flow is no longer a footnote – it’s a structural feature of the US M&A landscape.

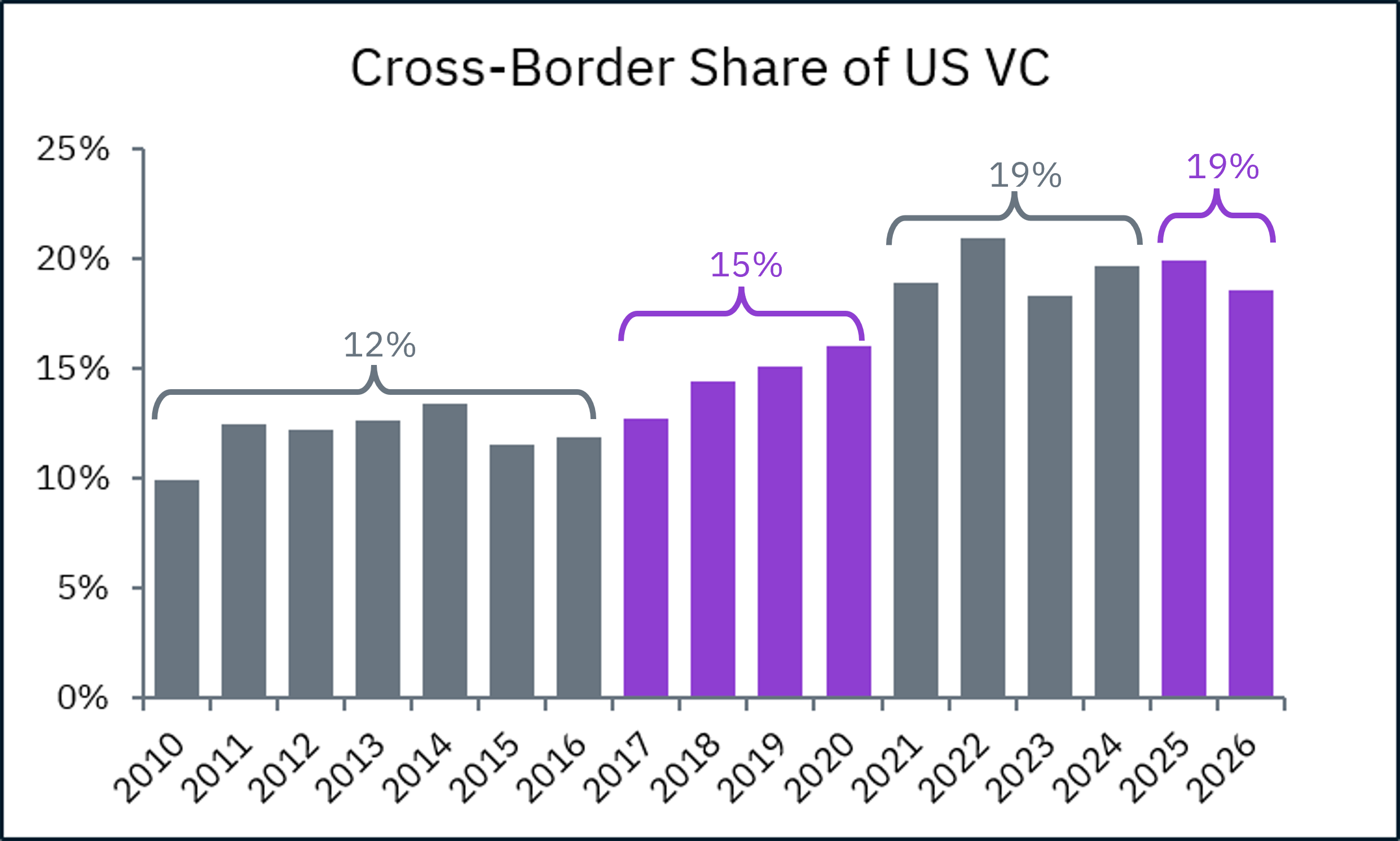

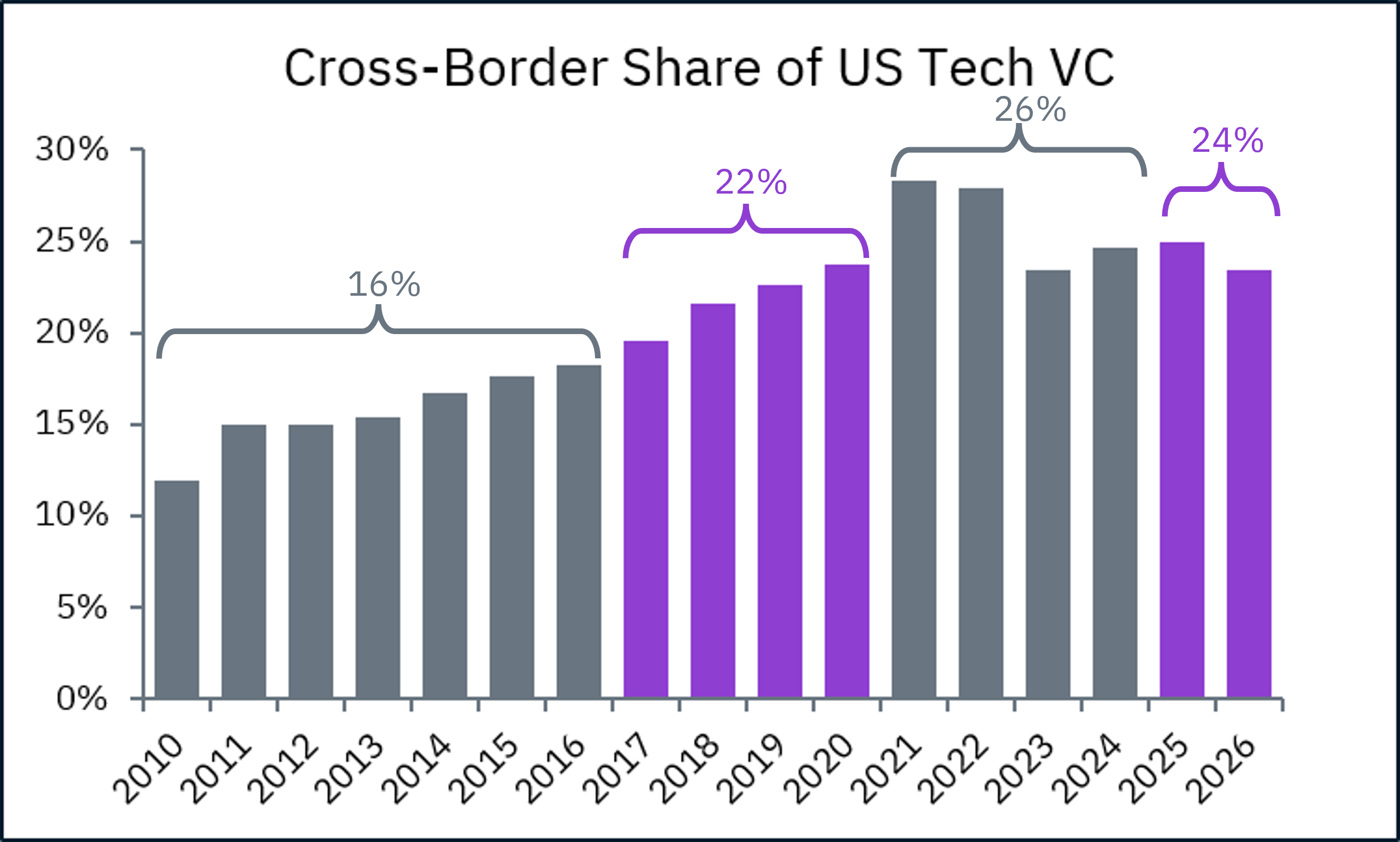

Next we looked at cross-border activity in US VC funding.

Here we see an already-growing trend accelerating under T1.0. Likely less to do with any Trump administration policies, and more to do with the rise of US unicorns, outgrowing domestic capital capacity and increasingly looking to the likes of Softbank, Tiger Global and Gulf sovereign funds.

Cross-border transactions have survived tariffs, trade wars, a pandemic, and two ideologically opposite Presidents. The demand for US companies – from Tokyo to Abu Dhabi – hasn’t wavered.

Administrations change. Policies change. Deals keep closing.