News

News

FTFL - 100 Days of Transactions

This article appeared in our May 2025 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

For our May FTFL, we write about what our readers tell us they enjoy the most. Now over 100 days into the Trump 2.0 Administration, we decided to “kick it old school” and write about current growth tech M&A and financing trends and what we think the data suggests for the balance of CY25.

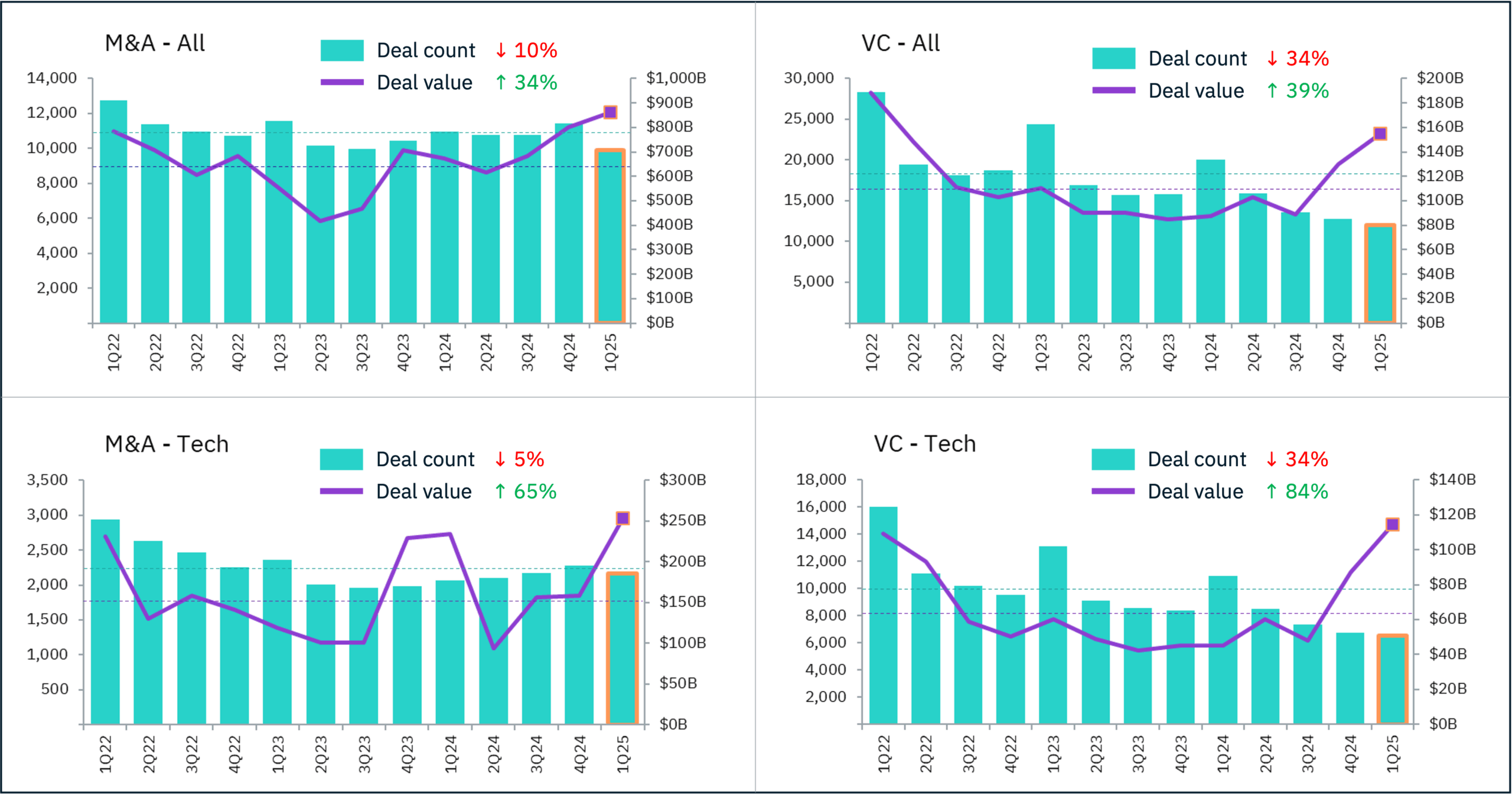

For this analysis, we’re focusing on 1Q25 stats and comparing them to the prior 12-quarter average, which gives us a lengthy normalized basis and excludes the 2021 peaks and pandemic valleys. For ease of reading, all graphs on the left relate to M&A statistics, and all graphs on the right relate to VC financing statistics.

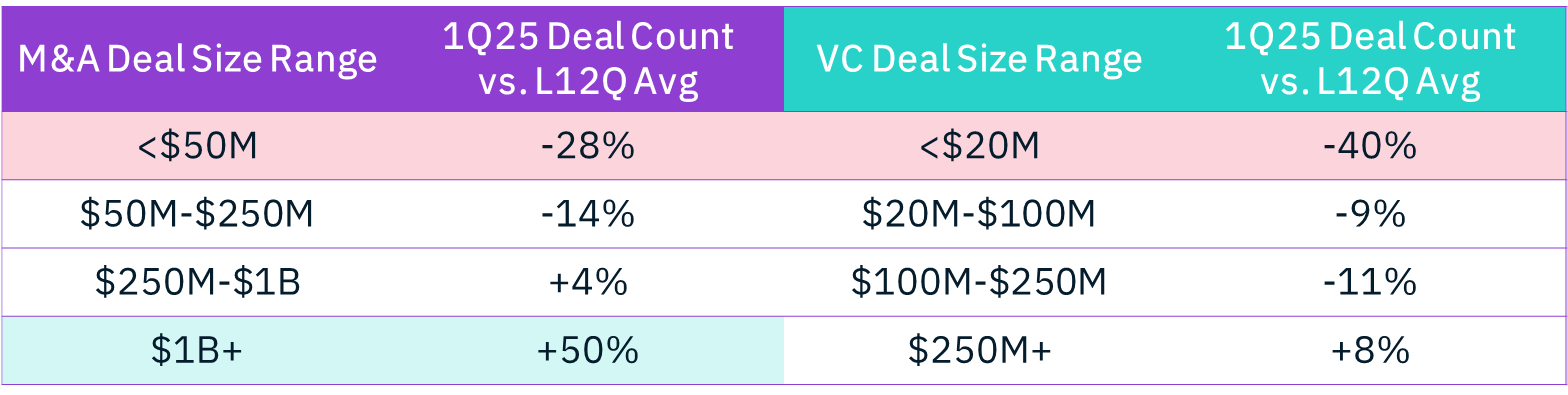

Deal counts are down while deal values are up – does that mean bigger deals are getting done at the expense of smaller deals?

On the M&A side, that’s exactly what is happening. The number of $1B+ deals in 1Q25 was the most since 2021, and the aggregate value of those deals was the most since 2018. Meanwhile, the deal counts and aggregate values of sub-$50M deals were the lowest since 2020.

On the VC side, megadeals appear to be relatively flat in deal counts. In fact, it’s a super-mega-ultradeal (trademark pending) that’s causing an anomaly – OpenAI’s record-shattering $40B funding. Excluding that one transaction, aggregate VC deal values in 1Q25 were up only 3% over the 12-quarter average. One area of concern is around the smallest of deals. Looking at seed and pre-seed deal counts, we found they are down 41% vs. average – which implies that new company formation is materially down.

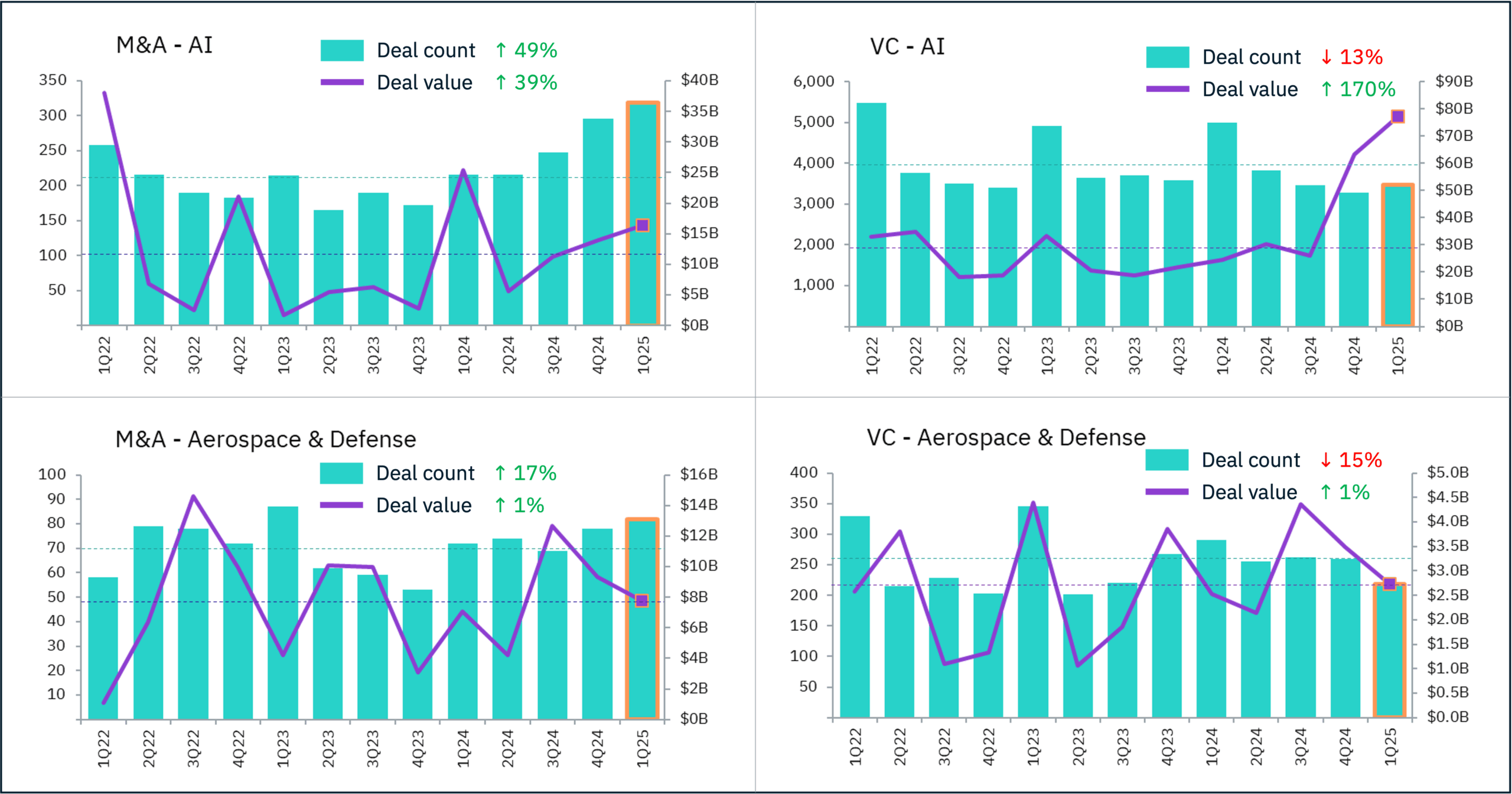

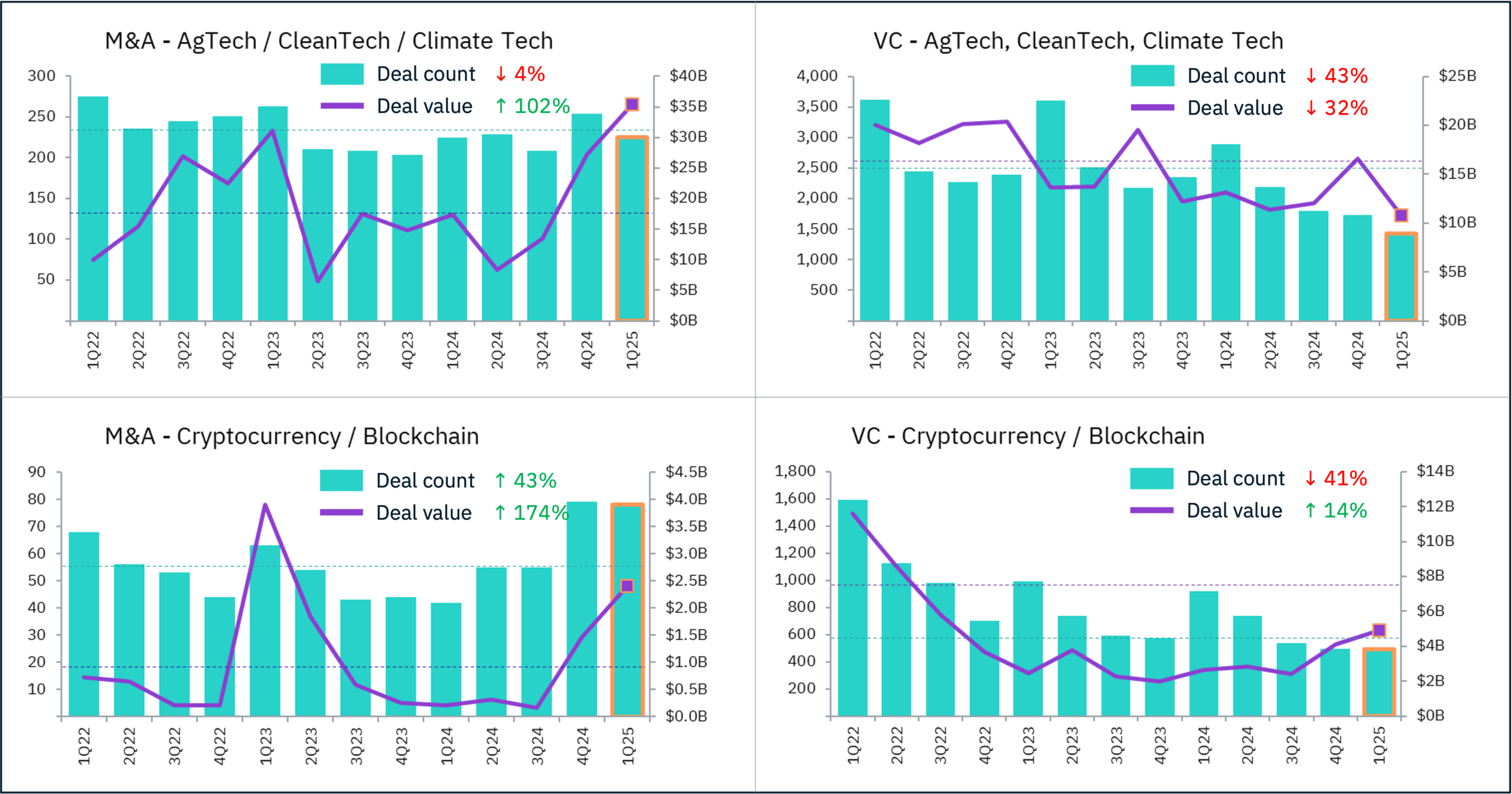

We dug into the market data some more, looking at trends across various sectors of interest to us. Our hypotheses:

- AI would keep going up, unaffected by any White House actions

- Expectation of increased defense spending would drive transaction volume

- The opposite would be true for sustainability tech

- Crypto-friendly administration would lead to increased deal activity

The results:

How did we do on our trend theories?

- AI – mostly right, but what stands out is that quarterly VC volume hasn’t changed much as deal values have grown. It’s really been the super-mega-ultradeals that have been driving AI VC growth

- Defense – not much movement. It may take a few more quarters to see any transaction momentum

- Sustainability tech – VC deals losing steam as expected, but M&A deals showing surprising resilience, confirming what our Sustainability team predicted earlier this year

- Crypto – as we discussed in March, the upswing already started in 4Q24, at least in M&A

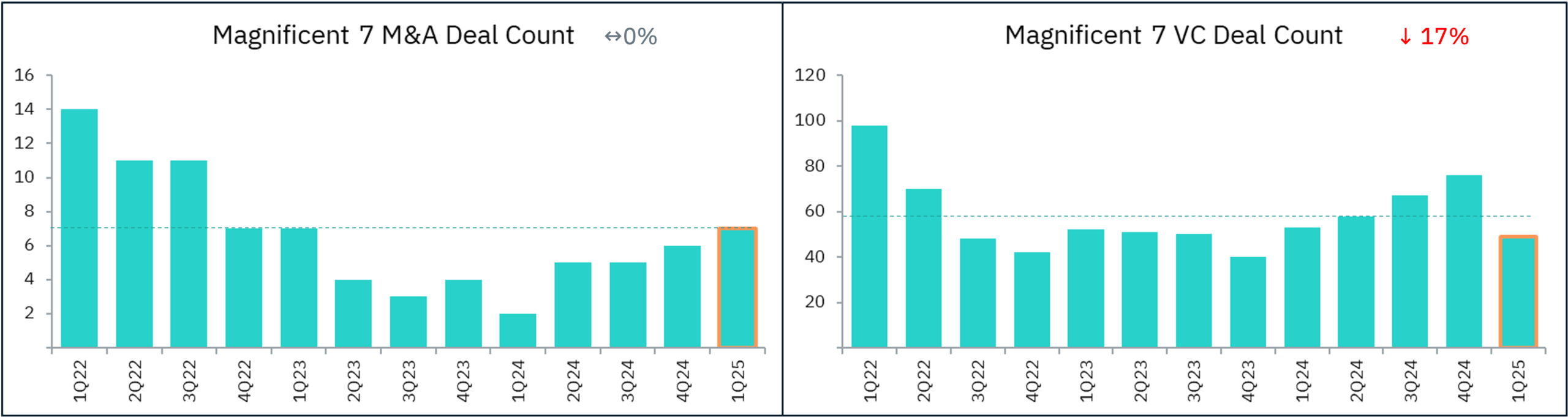

Finally, let’s check in on the Magnificent 7. We’ll focus on deal counts only, since their M&A deals are predominantly undisclosed values, and their VC deal values are driven by massive AI deal spikes.

It looks like business as usual for Big Tech, for now – M&A is at a normal pace, while VC counts are down only slightly.

While the Trump 2.0 Administration has “flooded the zone” in a clearly unprecedented manner, many of the key policy changes remain in limbo, most notably in tariff policy. We believe these new policies are so unsettling that they must be settled, quickly. As in 2Q25 quickly (sending Scott Bessent to Geneva was a good start). If this proves to be the case, 2H25 outlook leading up to November 2026 mid-term US elections should be all about the tech ecosystem positioning around AI. That positioning needs to focus on growth – both organic and inorganic.