News

News

FTFL - Oil Spikes, Growth Tech… Shrugs?

This article appeared in our April 2026 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

We love this FTFL journey we are on together. One of our readers praised our March correction prediction coming true, while noting we failed to predict the war in Iran as the causation. Tough audience – just the way we like it!

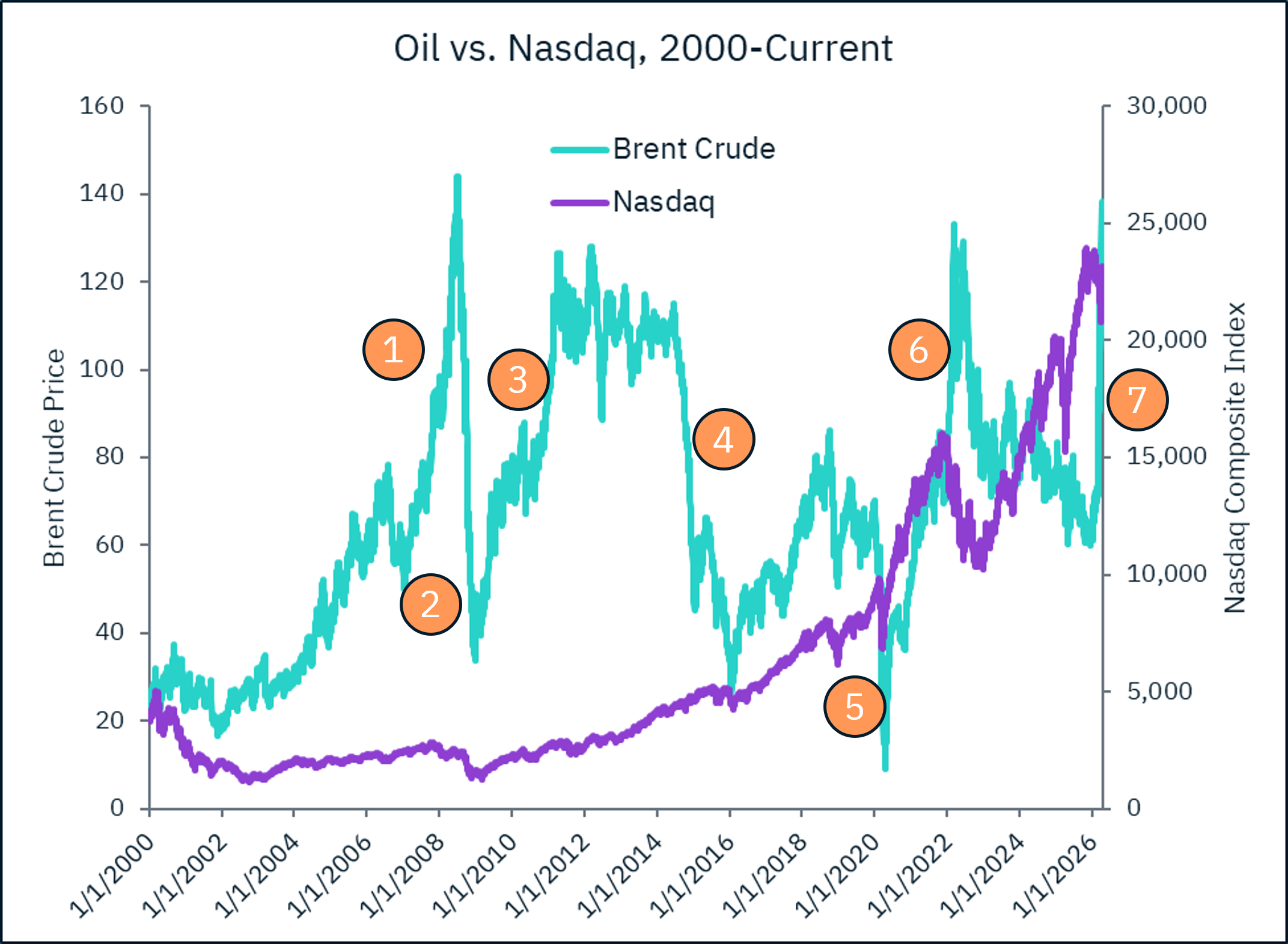

This month we dive into causation / correlation as it relates to the Iran war’s biggest economic impact – the price of oil. Brent crude has gone from $70 to as high as $138, as tanker traffic through the Strait of Hormuz has ground nearly to a halt, triggering one of the largest energy supply disruptions in modern history. What does an oil shock like this mean for growth tech?

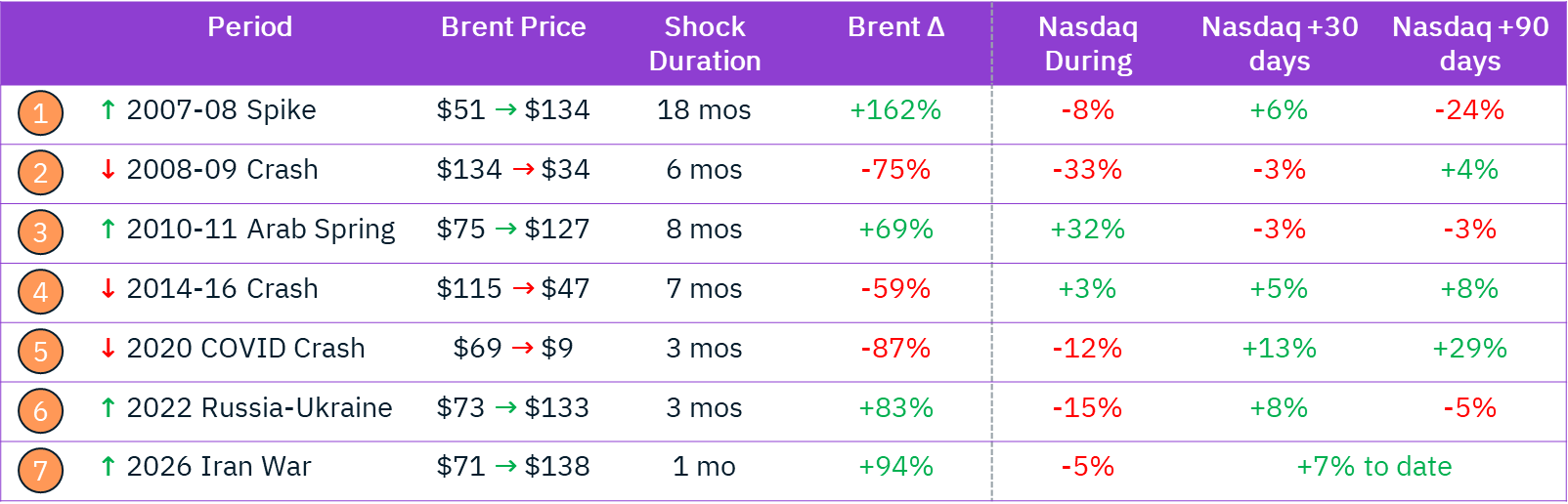

We started by looking at 25 years of Brent crude vs. the Nasdaq to see if there’s any clear relationship, then dug deeper and mapped every major oil shock since 2007 against Nasdaq performance during the shock and in the 30 and 90 days after.

Our entering assumption was that if oil goes up, Nasdaq would go down. But it turns out that oil shocks are not a primary driver of growth tech performance. When the Nasdaq moves meaningfully, it is almost always explained by something else. Focusing on major Nasdaq movements, the drivers are consistently macro or policy-driven, not energy-driven:

- Row 1: 24% drop at 90 days marked the onset of the Great Recession

- Row 2: 33% drop was the Great Recession deepening

- Row 3: 32% rise driven by the Fed’s QE2 program

- Row 5: 29% rise at 90 days was driven by the Fed’s COVID emergency intervention

Regarding the current shock in Row 7 – not only was our oil up / Nasdaq down assumption wrong, but note that the Nasdaq is currently trading near its all-time high, even as oil is up 94%.

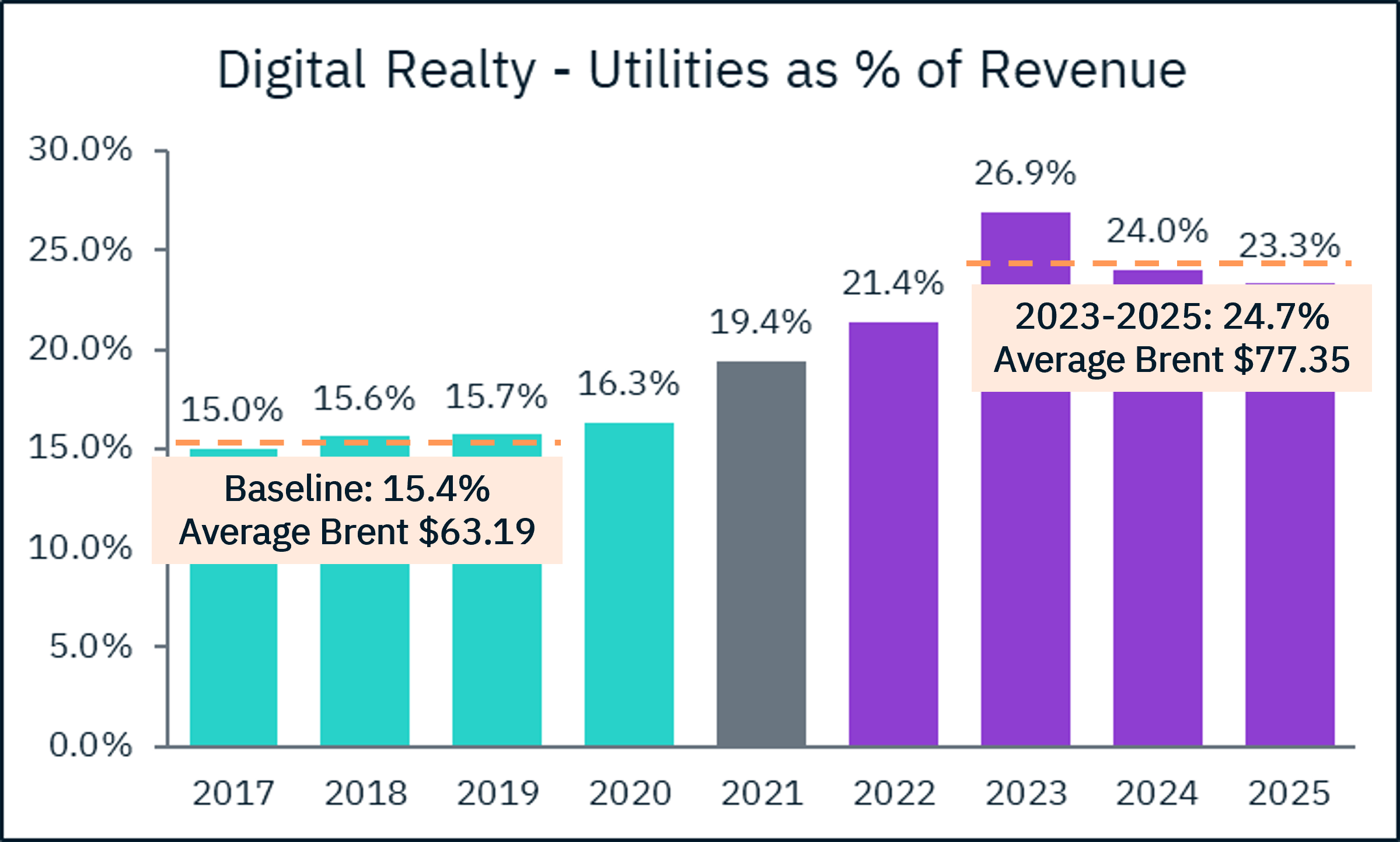

If oil shocks don’t meaningfully impact growth tech through valuations or market performance, the next question is: where do they show up? The answer is in cost structure. Higher shipping and transportation costs ripple through the global economy, as reflected in recent inflation data.

For growth tech, the most direct and measurable exposure is energy consumption, particularly in data centers. To isolate this effect, we turned to data center REITs – owners of the physical infrastructure underpinning the cloud. We used Digital Realty (DLR), the largest publicly traded player, which reports utilities as a standalone line item, allowing us to track energy cost pressure over time.

The Russia-Ukraine shock hit DLR’s financials with a 12-18 month lag – utilities as a percent of revenue increased nearly 1,000 basis points, even as oil prices had already pulled back from their March 2022 high.

This has significant implications for hyperscalers, whose projected $265B of capex growth this year will be driven by data center expansion. What could these companies do to mitigate unwanted energy bill increases? No idea is too crazy when you’re worth several trillion dollars.

- Vertical integration – i.e. become a utility

- Geographic arbitrage – move DCs to cheaper power regions

- Build a better mousetrap – more energy-efficient hardware and software

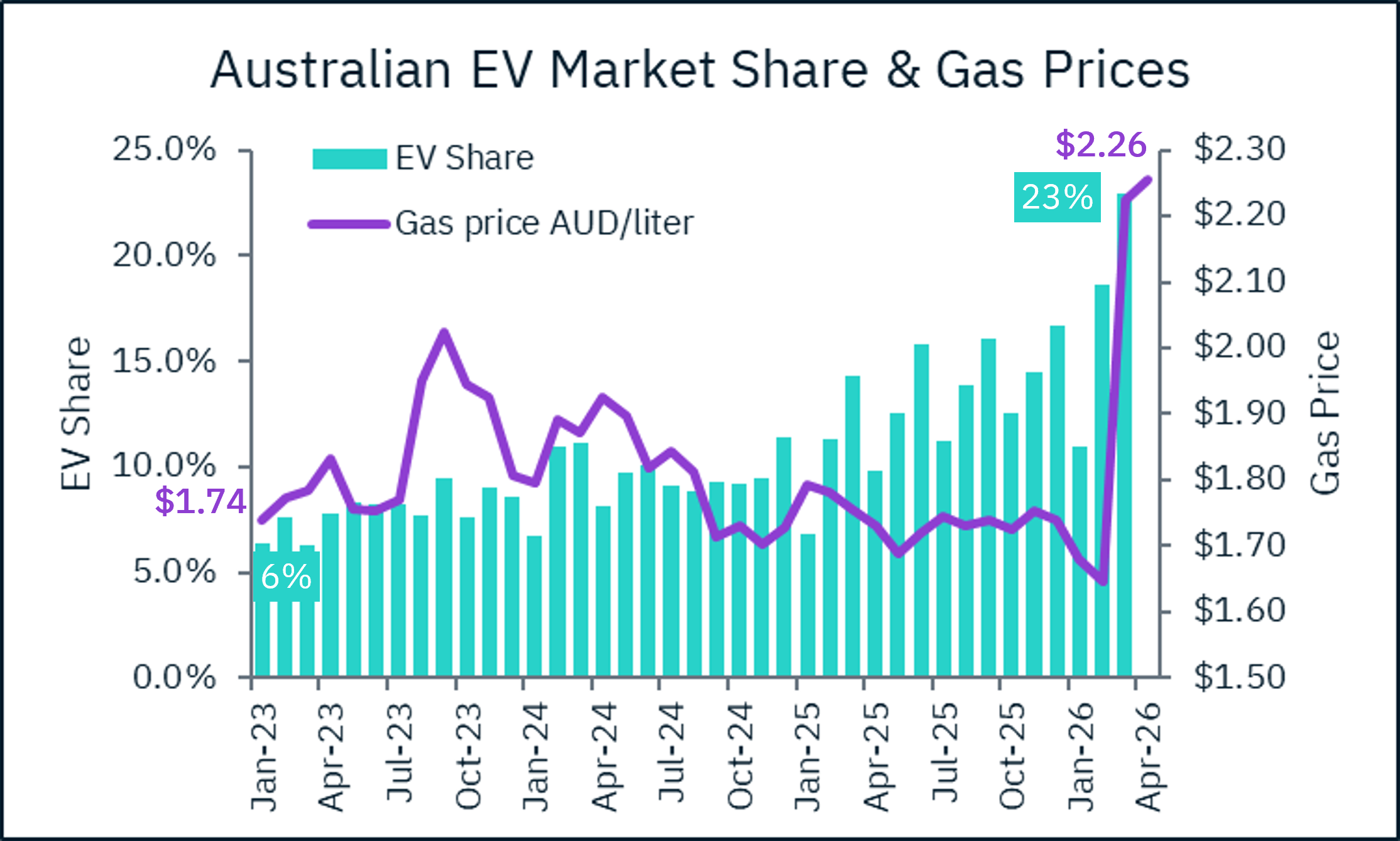

Beyond data centers, sustained increases in energy prices can also drive behavioral shifts – particularly toward alternative energy. To explore this, we looked at EV adoption as a real-time proxy for how consumers respond to rising fuel costs. However, for our purposes, we can ignore the U.S. market, as Q1 EV results showed that the recent growth of the market was entirely dependent on federal incentives, which ended on 9/30/25. Without the incentive, Q1 EV sales were down 27% year-over-year, despite gas prices up nearly 50% year to date.

Instead, we focused on Australia, where monthly EV sales are reported quickly and policy has remained relatively stable, allowing for a cleaner read on the relationship between gas prices and EV adoption (and yes, the U.S. EV market is ~20x larger, but the directional signal is our focus here).

March EV sales reached an all-time, with EV share rising to 23% of all new vehicles sold in Australia, while gas prices jumped 35%. With prices continuing to rise this month, we will be curious to see how April EV numbers shake out. And in the longer term, if Australian gas stays above AUD $2.00 per liter, we think EV share will remain meaningfully above 20%.

While oil shocks don’t dictate how growth tech trades, the real effect is in behavior change – from how tech gets built, to how it gets powered, to ultimately how it’s consumed.

James Carville once famously said, “It’s the economy, stupid.”

We offer you, “It’s the price at the pump, stupid.”