News

News

FTFL - Hyperscalers Are Buying GPUs. SaaS Is Buying Back Stock.

This article appeared in our March 2026 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

The opening quarter of 2026 has seen a blistering news cycle, headlined by the war with Iran.

For March, we explore corporate capital allocation strategies and their importance for the broader growth tech ecosystem. Fair warning to readers, what has historically been considered a sleepy topic is quickly becoming a leading indicator.

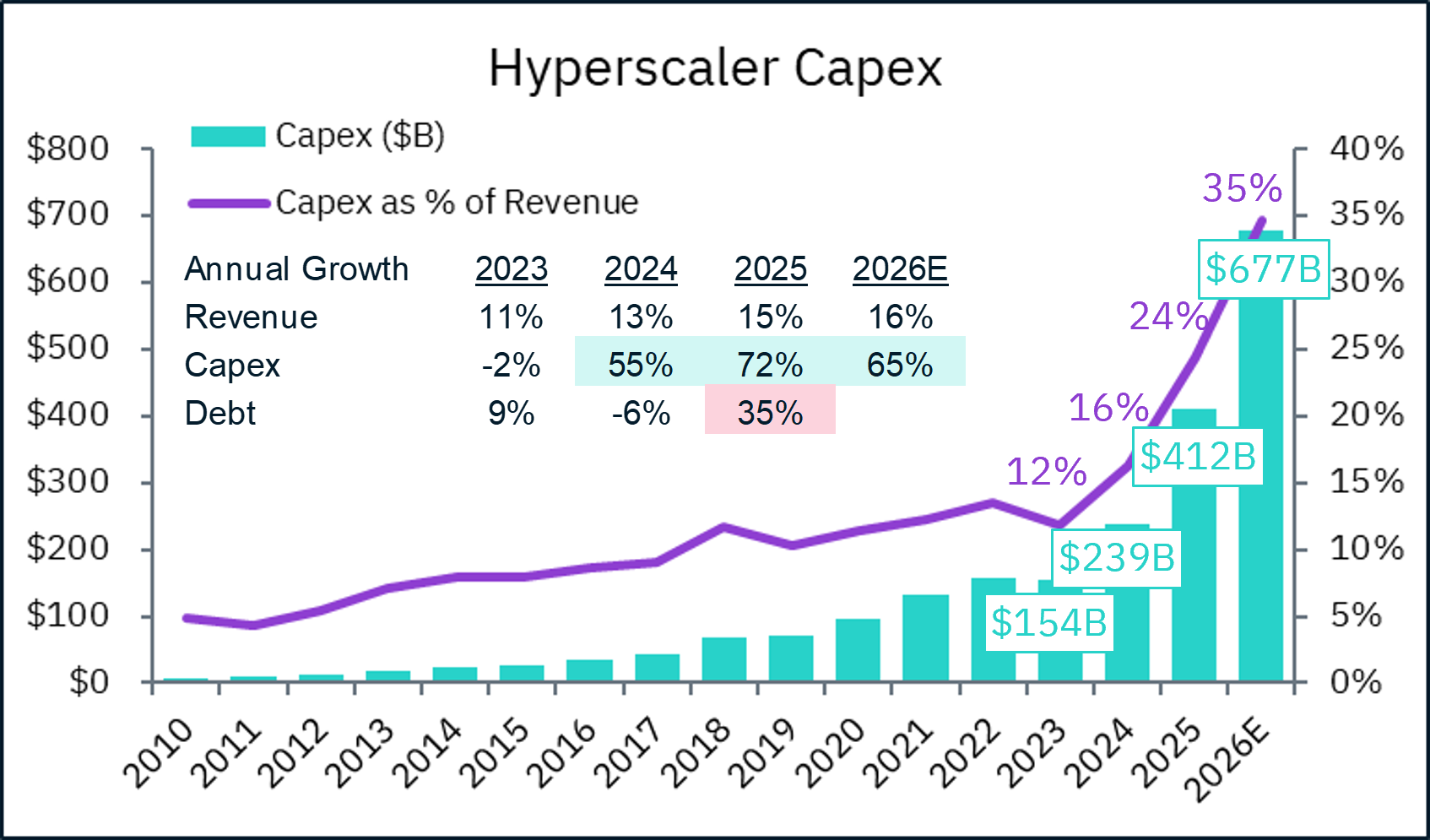

We start at the top of the food chain and the top of everyone’s mind – hyperscalers and AI. For this analysis our group includes Amazon, Google, Microsoft, Meta and Oracle. While these hyperscalers do not explicitly break out AI spending, public commentary and analyst estimates indicate that well over half of recent hyperscaler capex is now tied to AI infrastructure. We know capex has surged to support AI and data center buildouts, but by how much?

Whoa. That is a Gretzky-level hockey stick. Capex grew by 72% in 2025 and is projected to grow 65% this year, compared to revenue growth of 15% and 16%, respectively. Further, aggregate capex is estimated to represent 35% of revenue in 2026, a level never seen by this group, and more commonly associated with chip companies like Intel, TSMC or Micron.

Note the 35% growth in aggregate debt in 2025 on the heels of a 6% contraction. A $170B capex increase followed by an expected $265B increase has to be funded from somewhere, and as we’ll see in chart below, raising debt is only part of the story.

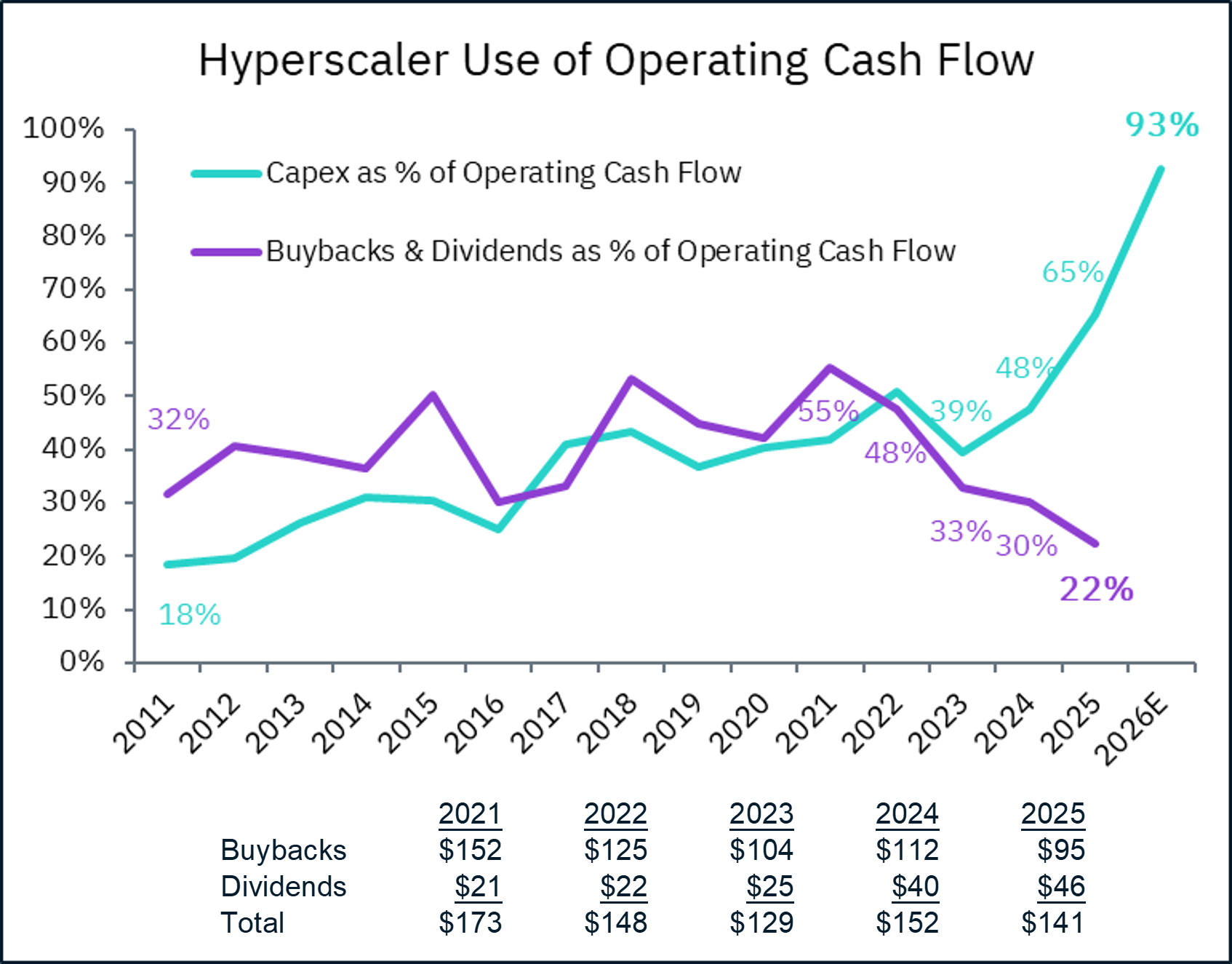

These wildly profitable companies are effectively spending all their profits on AI, with capex expected to reach 93% of operating cash flow this year. The hyperscaler AI bonanza appears to be coming at the expense of capital returned to shareholders, as share buybacks and dividends have decreased over the last 5 years from 55% of operating cash flow to 22%. Looking at dollar amounts, dividends have consistently increased year-over-year, while buyback spending is down 38% since 2021.

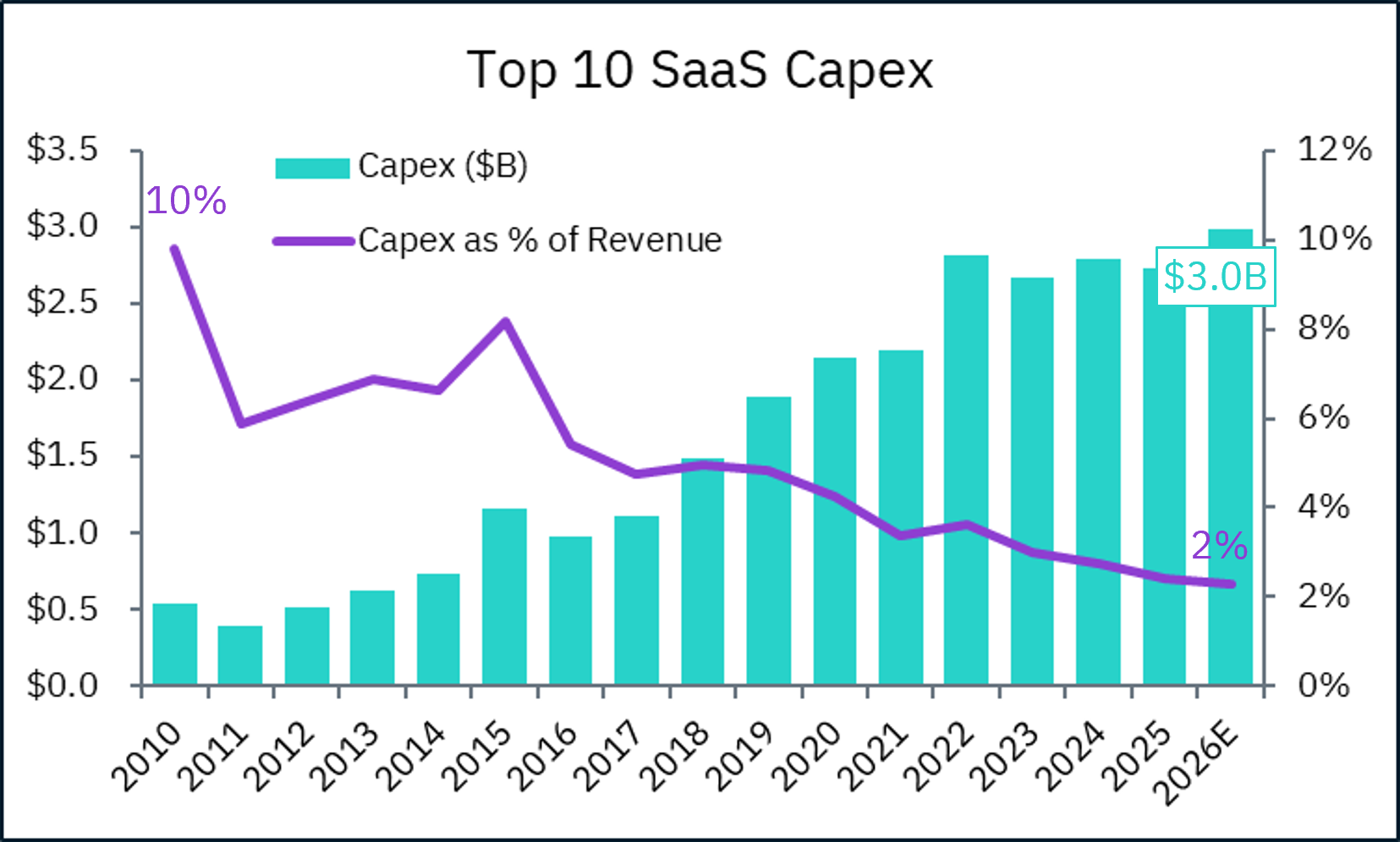

Now let’s look beyond the hyperscalers. If you read our piece last month, you’ll remember we examined the SaaSpocalypse via a Top 10 SaaS list, whose stock prices were down 29% YTD at the time (currently down “only” 22%). Let’s see how this group has been allocating capital over the past 15 years.

Capex for this group has decreased from 10% of revenue to 2%. Such a low level of capex should come as no surprise for an industry famously built on AWS, GCP and Azure – the ability to use public cloud services to support growing infrastructure needs is a big reason SaaS companies proliferated throughout the 2010s. This group is clearly allocating cash flow elsewhere…

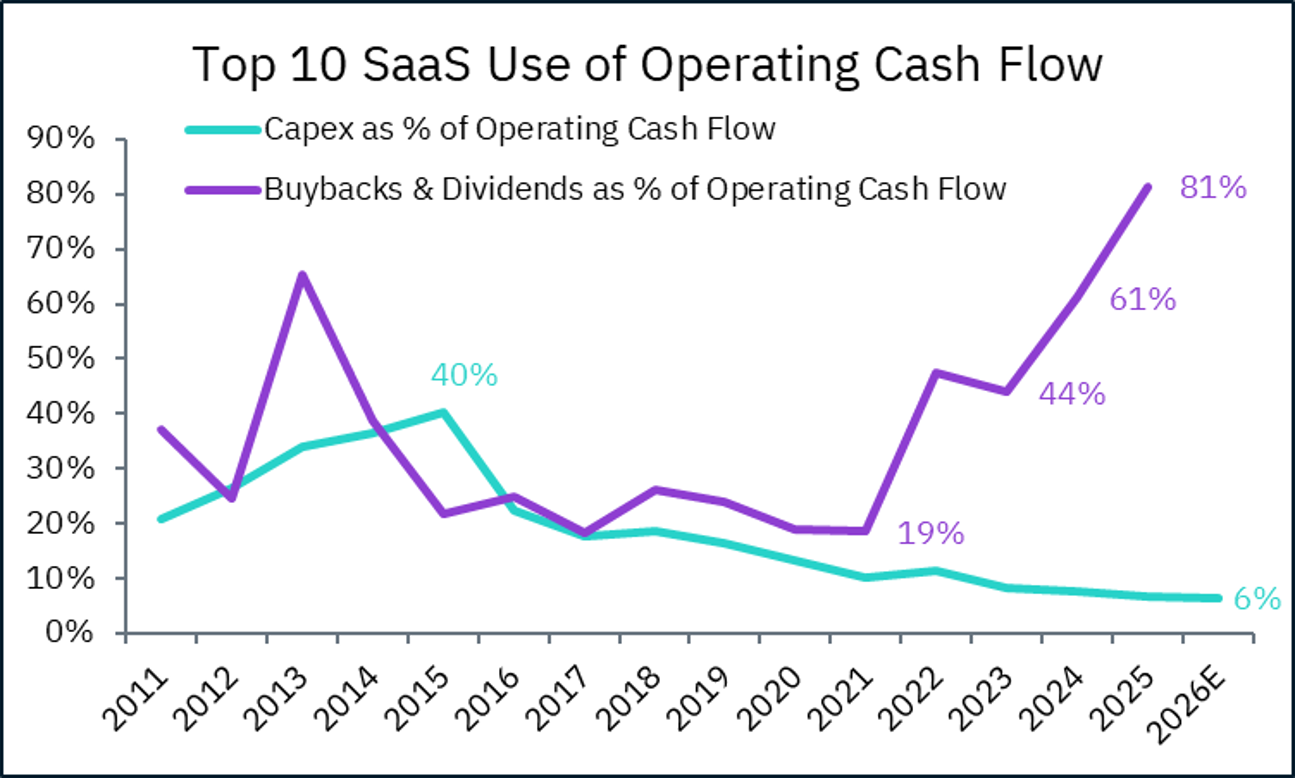

This is essentially the inverse of the hyperscaler chart, with capex as a percent of OCF decreasing from 40% to 6%, while over the last 5 years, dividend & buyback percentage of OCF has skyrocketed from 19% to 81%. And headlined by Salesforce’s $50B buyback announcement, we think that figure will keep going up this year (one growth tech truth that has stood the test of time: when you ain’t growing topline and bottom line, you turn to reducing share count).

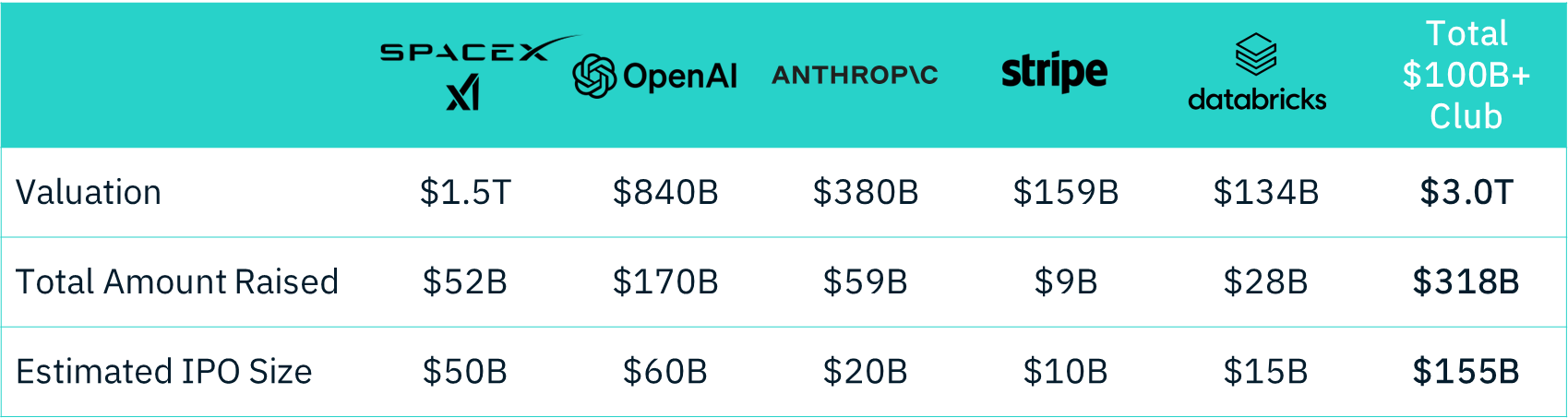

We’ll finish our allocation tour de force with one of our favorite topics, unicorns. Actually, decacorns. Actually, hectocorns. 2026 may finally be the year the IPO dam bursts, with the largest private companies rumored or publicly indicating their intentions to go public as soon as this year. For this part of the analysis, we’re focusing on the $100B club.

These 5 companies have raised in aggregate $318B in VC funding. They represent one-third of all US VC funding since 1/1/24 (including 71% of all US VC funding this year to date!).

Aggregate estimated IPO size for this cohort is $155B, equivalent to the last 4+ years combined of all US IPOs.

This sets up a significant reallocation of capital across the growth tech ecosystem. Capital is already rotating out of public SaaS – accelerated by the recent sell-off – as investors position for $150B+ of upcoming IPOs. Following these listings, lockup expirations could release up to $318B of capital back into the market in 2027, setting the stage for the inevitable next investment cycle.

The question isn’t whether that capital will be redeployed, but where it will go next.

Quantum computing bubble, anyone?