News

News

FTFL - EO Effect on Tech

This article appeared in our March 2025 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

Breakneck, unprecedented, relentless… we’ve heard a lot of descriptions of the pace of executive orders. 89 in the first 51 days and counting. No, we haven’t pivoted our newsletter focus to politics. We’re just curious – what might these actions mean for growth tech?

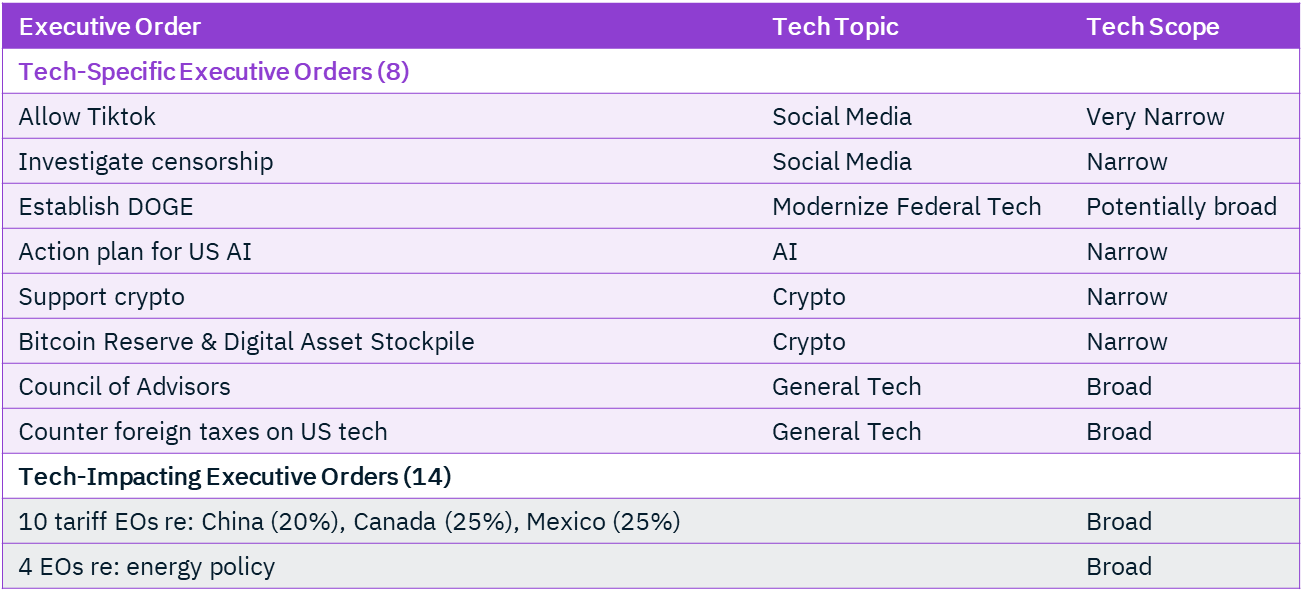

Of the 89 executive orders, we found 8 that specifically referred to areas of technology.

While DOGE could have long term lasting impacts and TikTok got a 75-day stay of execution, let’s jump to a couple of EOs that don’t specifically call out technology, but have already had reverberations across the tech world: the 20% increase in China tariffs.

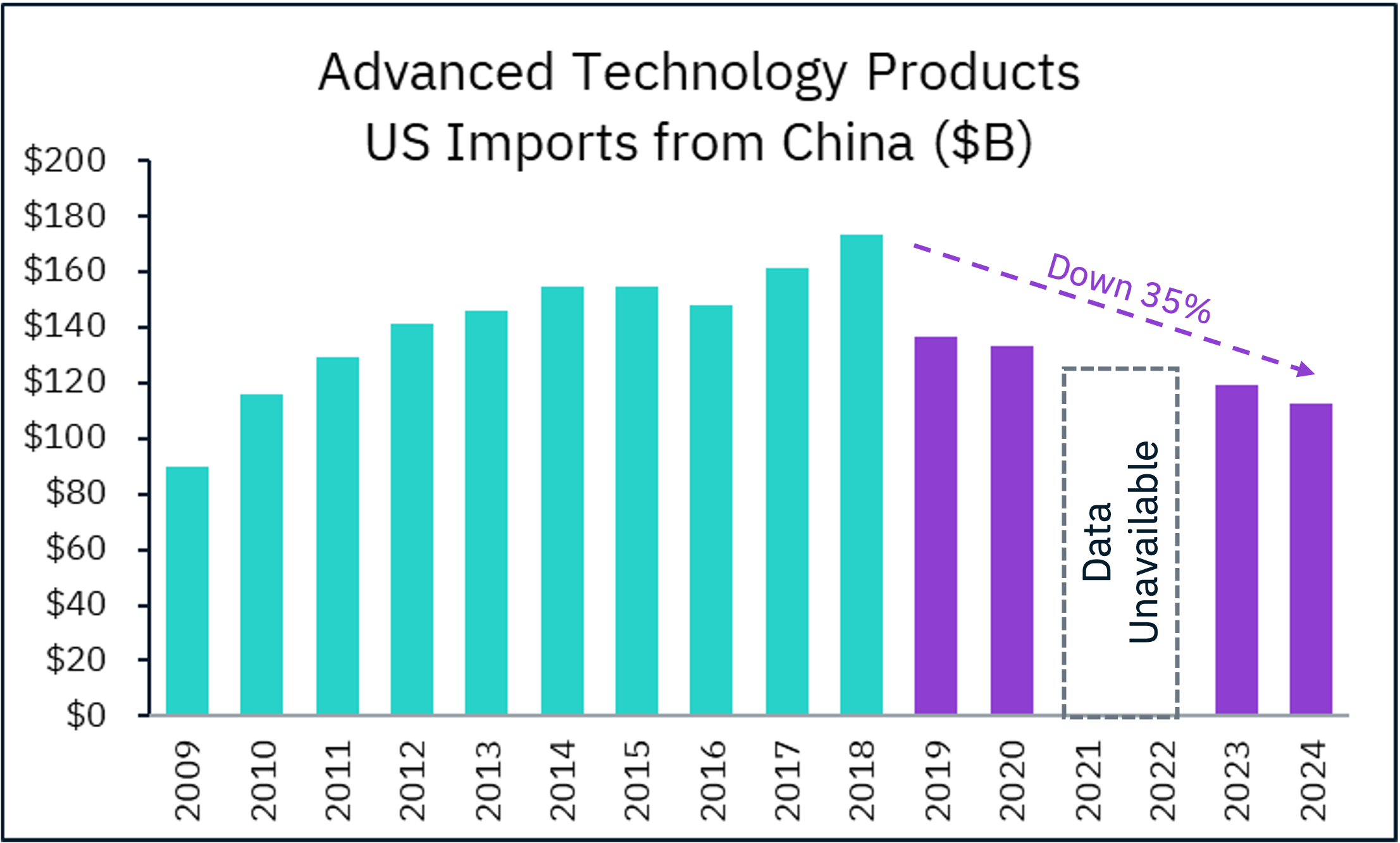

On February 1 and March 3, the White House issued executive orders that each added 10% to the existing 7.5% tariff on all goods exported out of China, bringing the total to 27.5%. This was anticipated by the tech community – preparations for increased tariffs had begun after Election Day, with companies attempting to accelerate Q1 shipments and move operations out of China. And if we look at data from the US Census and US Bureau of Industry and Security, we see that the tech industry has already been decreasing business with China for a while, with 2024 advanced technology product imports from China down 35% over the last 6 years, reaching its lowest level in 15 years.

What started this trend? Huawei. In 2018 the US determined Huawei telecom gear to be a cybersecurity threat and barred the federal government from purchasing its products. What followed suit has been a larger exodus as the US attempts to decrease its economic reliance on China.

As a result, many US tech vendors have spent the last several years migrating their manufacturing to Vietnam, Thailand, Malaysia, India and Taiwan. But this move has not been a simple fix. China has had a 20-year head start as global leaders of the tech supply chain, and tech vendors have discovered several challenges with migrating to other countries, including:

- Higher cost of labor outside of China, even in other “low-cost” countries

- Shortage of technical expertise in areas such as CAD/CAM, semiconductor packaging, and high-density PCB fabrication

- Limited production capacity and scale

- Port congestion and longer shipping lead times

The impact has been immediate and it began on February 1. The additional cost of either doing business in China or moving out of China creates a decision spectrum for all affected companies: increase prices at the risk of losing customers vs. take the margin hit at the risk of harming profitability and/or cutting costs elsewhere. This is an extremely difficult balance and we believe approaches to these competing pressures will play out over the ensuing quarters.

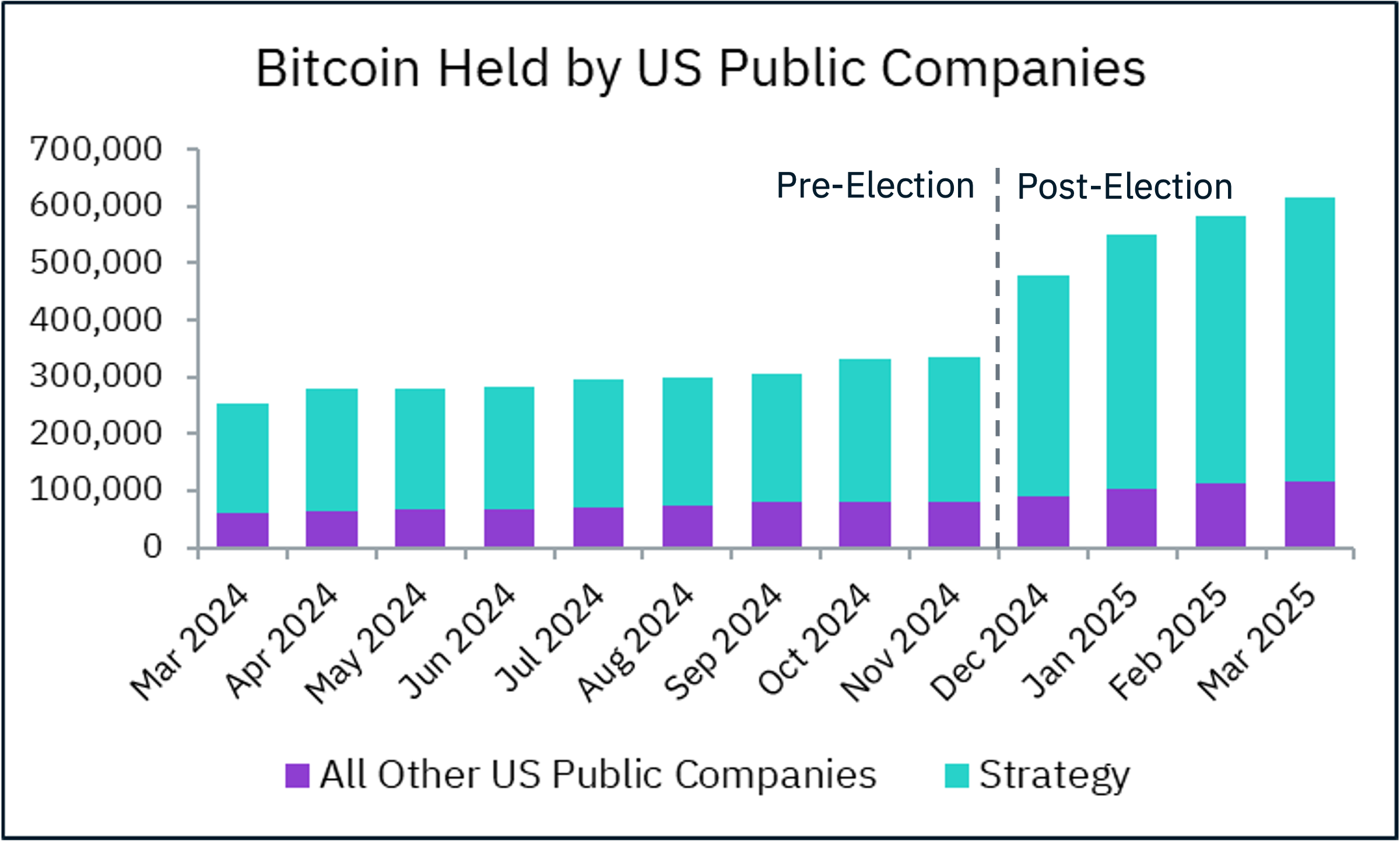

Another EO we found interesting was issued on January 23 and stated the administration’s intent to support digital currency and blockchain technology (i.e. cryptocurrency), and re-evaluate existing crypto regulations. And just last week, a new executive order established a Strategic Bitcoin Reserve and Digital Asset Stockpile.

These EOs aim to validate the underlying worth of cryptocurrency and underscore an ongoing trend: Bitcoin gaining acceptance among CFOs as a legitimate treasury asset. According to data from BitcoinTreasuries.net, 27 US public companies now own Bitcoin, up from 19 a year ago.

Over the last 12 months, US public company Bitcoin ownership, excluding Strategy (formerly known as Microstrategy), has gone up by 89%, from 62,000 coins to 117,000. Meanwhile, Strategy’s Bitcoin ownership rose steadily during most of 2024, but then has nearly doubled since Election Day. Similar to the China tariffs, anticipation of the EO has fueled change before the EO itself.

Adverse to owning crypto? Well, between the 27 Bitcoin-holding companies and Strategy recently being added to the Nasdaq 100, if you own any mutual funds or index funds, you likely already own some Bitcoin, regardless of your opinion of Michael Saylor’s “strategy.”

Only 51 days in, these executive orders stand to reshape the global economy. Early returns are Big Tech’s relative immunity may be wearing thin – note that over the last month, the Nasdaq is down 11%, while the Magnificent 7 have lost $2.2 trillion in value. Where is all of this headed? For the first time in a long time, it appears that Big Tech’s crystal ball is starting to look cloudy.