News

News

FTFL-GE: Is Software Sustainable?

February 2025 issue of From the Front Lines (Green Edition), Bowen’s dedicated sustainability sector newsletter, spotlighting tech trends and insights in Agriculture, Water and Waste, and Energy.

In 2011, Mark Andreesen famously said, “Software is eating the world.” In this edition of FTFL-GE, we’ll take a look at how that applies to two of our sustainability segments – agriculture, and water and waste. We’ll save energy for a future edition, as we see different dynamics there. We did our analysis by looking at some major 2024 exits in each space to see what role software plays.

- Does software play a role at all?

- Is the company essentially software-only?

- Does the company bundle software with other hardware or services to provide an integrated solution?

Let’s start in agriculture. Our thesis was that most farmers and agriculture-related problems will require hardware or services to complement the software and that software-only companies would generally find it more difficult to scale.

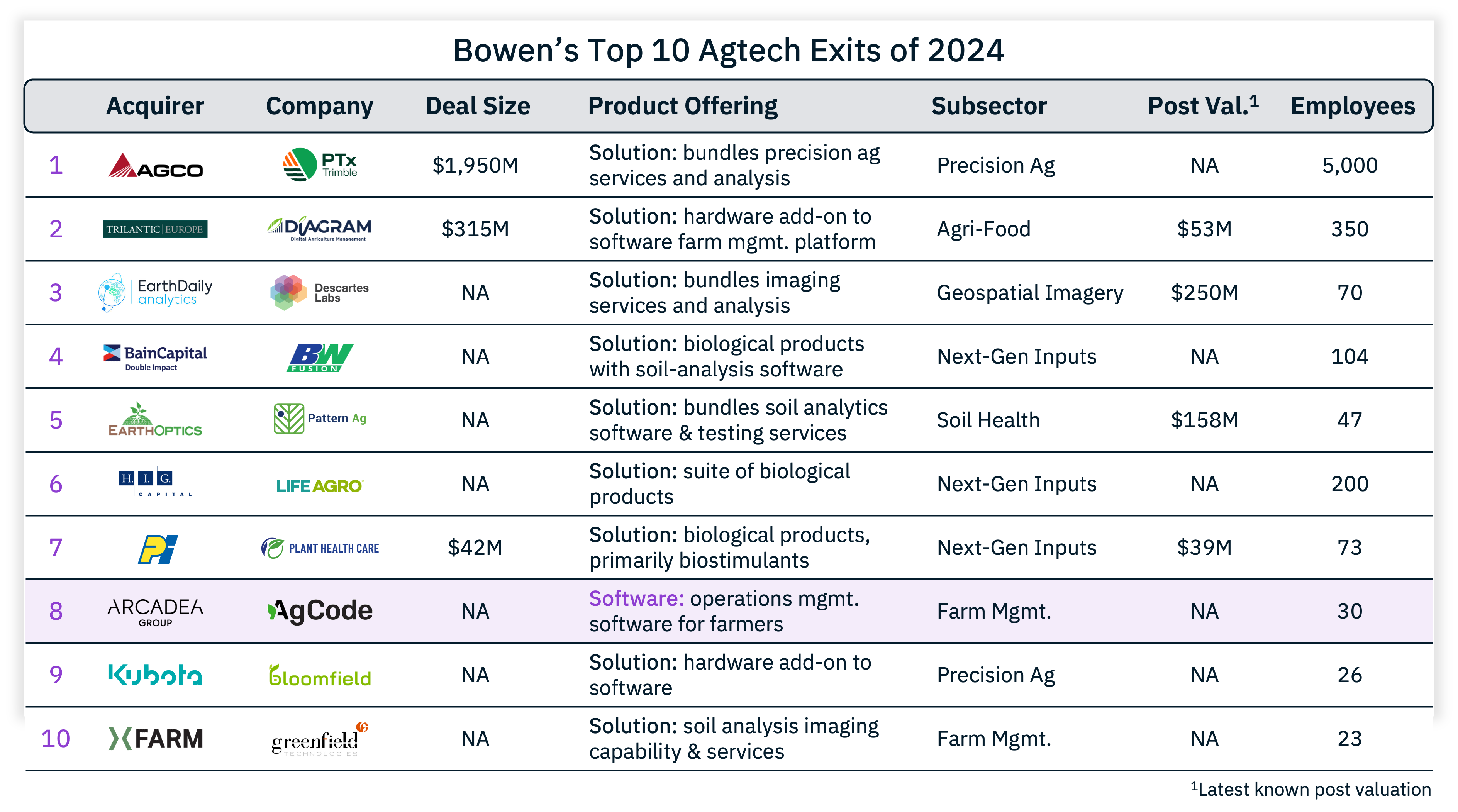

Here are Bowen’s top 10 ag tech exits from 2024, within our core practice focus areas. For this exercise, we separated product offerings into three categories: solutions, software, and services. Solutions encompass any mix of hardware and software alongside pure product-driven companies; software encompasses pure-play software companies; and services encompass companies with pure service offerings. Financial data was unavailable for most of them (or in the case of BW Fusion, it has not been published), but we chose them using other available metrics, such as number of employees, last-round valuation, and quality of their backers.

Only one of the 10 was a pure software play. In others, hardware or services are a key part of the solution. Of those 10 deals, only AgCode, which is operations management software (think SAP for farms) is a pure software company. Descartes Labs bundles imaging services and analysis. The acquisition of Bloomfield Robotics by Kubota represents a hardware add-on to what is basically a software company. Similarly, the acquisition of Greenfield by xFarm added soil analysis imaging capability and services to xFarm’s software platform. As an aside, though, we consider xFarm to be one of the few software-focused companies in agriculture that has successfully scaled organically, although they are now embarking on an acquisition strategy as well.

Is the story any different in water and waste? Not really. In fact, the situation is even more stark for software. Of Bowen’s top ten exits, none were software companies. Most were solutions to a specific problem, typically with hardware and disposable elements, such as Stericycle, or pure services.

It seems the vast majority of buyers are looking for solutions that may or may not include software. Pure software makes sense for operations management, but outside of that, it’s rare to find a scaled pure software solution in either agriculture or water and waste. More likely, you’ll see an aggregation of smaller niche products, such as Ever.ag, the Banneker Partners platform company. Analytics is a natural fit for software, but getting the data to analyze is probably going to require either services (like soil sampling for agronomy) or hardware to measure something.

Interestingly, the Wall Street Journal published an article this week (see link below) noting that even Oracle’s Larry Ellison, one of the most successful software entrepreneurs in history, has struggled in agriculture. His Sensei Ag has absorbed an estimated $500 million of his own money with little to show for it to date.

Flipping the analogy around, perhaps software is the appetizer in sustainability. Hardware and services are generally needed to make a meal.

What We’re Reading

-

Larry Ellison’s half-billion-dollar quest to change farming has been a bust | The Wall Street Journal

From the Front Lines by :

Bob Fleming

Managing Director