News

News

FTFL - Hot Summer, Cool Deals?

This article appeared in our July 2024 issue of From the Front Lines, Bowen’s roundup of news and trends that educate, inspire and entertain us. Click here to subscribe.

As we approach the dog days of summer, we thought it might be insightful to analyze data that will foreshadow what we believe will be a busy fall racing towards the end of the 2024 transaction season.

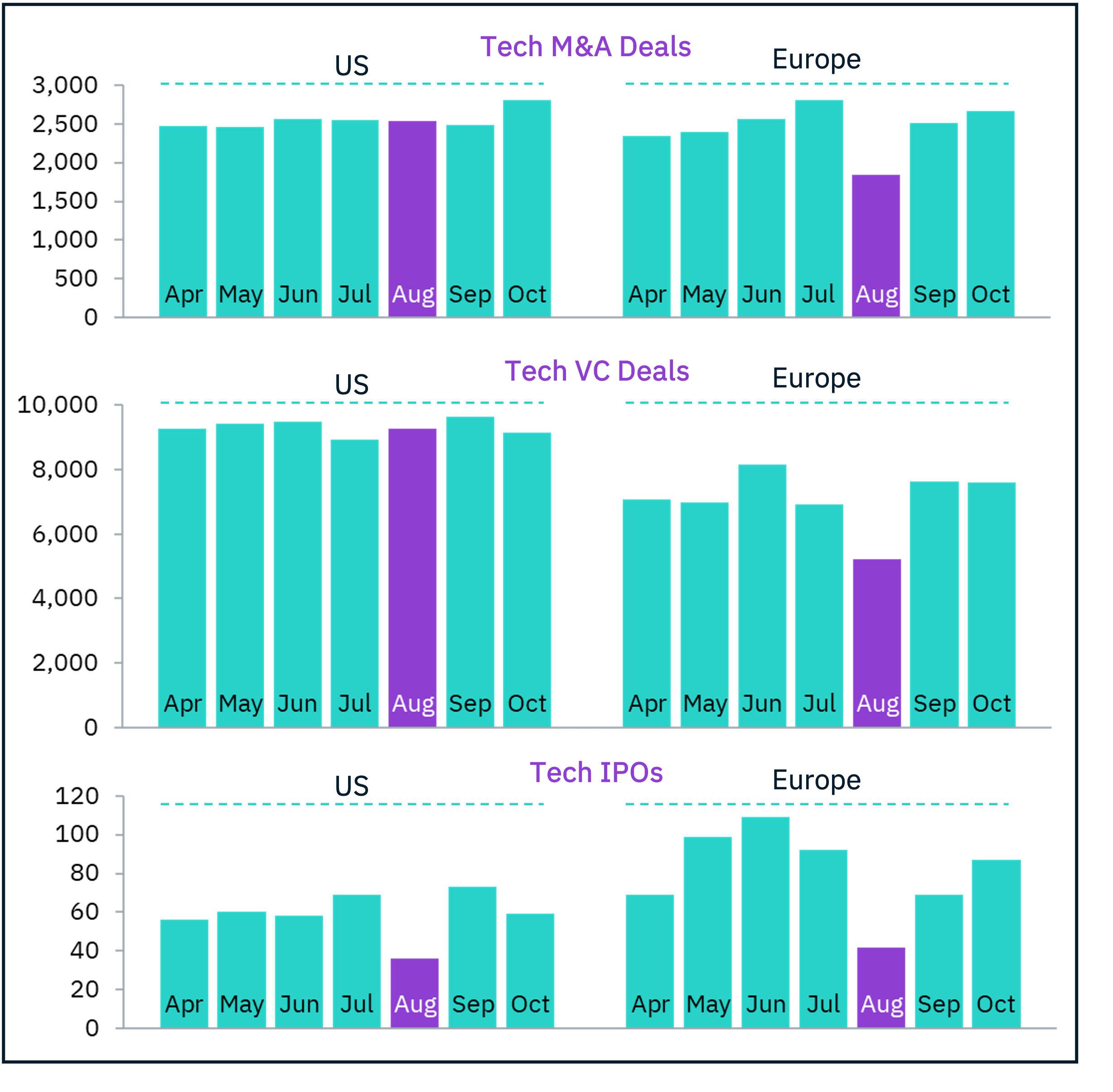

Summer Slowdown. Do growth tech capital markets slow down in the summer? Most tech investment bankers advise clients that the summer months, particularly August, are a dead time for M&A, capital raising and IPOs. Whether or not this is self-fulfilling as we bankers wish to take vacation, is it actually supported by the data? Well, it depends on where you live.

Based on the last 10 years of data, there is no evidence of a summer slowdown in M&A and VC here in the US. But in Europe, they know how to summer properly, with August deal volumes dropping 27% vs. prior months. We at least treat the IPO market appropriately, with a 41% August decline in the US and 54% decline in Europe.

Happy New Year(s). At Bowen, we tend to think about two “new years” in tech M&A: January 2nd and the Tuesday after Labor Day. Do more companies really come to market in January and September? To answer this, we looked at our internal data, tracking sellside process launch dates over the past 5 years.

January actually had the least amount of process launches, while April, May, June and September had the most. The April-June trend (48% of the total) makes perfect sense, as Boards and investors often target transaction closings by the end of the calendar year, with the average process taking ~6 months.

Bridge to ??? At Bowen, we are encountering a heavy dose of venture-backed companies that are in some form of bridge financing. We don’t think of bridges as inherently good or bad, rather we think about how the company reached this place.

At a macro level, how we got here is clear. If you track our prior FTFLs focused on VC liquidity, investors are being forced to make not-so-easy funding decisions. Absent a new lead investor where the bar continues to be incredibly high, an around-the-table, insider-led bridge financing just makes common sense.

What is unusual this time around is just how prevalent bridges are – including for $10M ARR to $25M ARR companies with strong, but perhaps not breakout, growth profiles.

Based on data from our friends at Pitchbook, the number of bridge loans to VC-backed tech companies has increased dramatically, more than doubling from 2018 to 2023. As a percent of all tech VC deals, the rate has nearly doubled as well, from 1.3% five to ten years ago to 2.4% today.

So where does it all end? Are these companies bridging to a permanent financing, a trade sale or just more bridging? We looked at the current status of VC-backed tech companies that received bridge financing.

If the past is any indication, then over time we should expect about 1/3rd of these companies will remain private, 1/3rd will have an exit, and 1/3rd will go out of business.

When we dug into the data even further, we found that 10% of companies that were bridged 5-10 years ago eventually required additional bridge financing in the future. While this modest re-bridge rate indicates a strong level of historical VC discipline, we find ourselves wondering, given the doubling of the rate of bridge rounds as noted above, will the re-bridge rate double as well?

At Bowen, whether it’s August sluggishness or September’s rush, we stand ready to ensure that your bridge leads to somewhere exceptional.